Theory

Some of the rates related formulas are from Leif Andersen’s 3-volume book.

[1]:

import IPython; IPython.display.HTML('''<script>code_show=false; function code_toggle() { if (code_show){ $('div.nbinput').show(); } else { $('div.nbinput').hide(); } code_show = !code_show} $( document ).ready(code_toggle);</script><form action="javascript:code_toggle()"><input type="submit" value="Click here to toggle on/off the raw code."></form>''')

[1]:

Automatic Differentiation Example

把數學函數全部重新定義一遍,output type 不用 float 而是用一個新的 class(Variable)同時存下數值(data)和導數(grad)

等於把本來的 \(\mathbb R \mapsto \mathbb R\) 函數都變成 \(\mathbb R \mapsto \mathbb R^2\),同時輸出點值和導數

Variable class 超載所有 arithmetic operator 把微分規則寫在裡面(如萊布尼茲公式)

在自定義的數學函數裡手動給他們的導數,例如 \begin{align*} \frac{d}{dx}\sin(x) = \cos(x),\qquad\frac{d}{dx}\cos(x) = -\sin(x). \end{align*}

Nothing is symbolic

[5]:

import math

class Variable:

def __init__(self, data, grad):

self.data = data

self.grad = grad

def __add__(self, other):

res_data = self.data + other.data

res_grad = self.grad + other.grad

return Variable(res_data, res_grad)

def __mul__(self, other):

res_data = self.data * other.data

res_grad = self.data * other.grad + self.grad * other.data # Leibniz rule

return Variable(res_data, res_grad)

def __repr__(self):

return f'data: {self.data}, grad: {self.grad}'

def sin(x):

return Variable(math.sin(x), math.cos(x))

def cos(x):

return Variable(math.cos(x), -math.sin(x))

def f(x):

return sin(x)*cos(x) + cos(x)*sin(x) # equals sin(2x) with derivative 2 cos(2x)

f(3.1415926) # expecting point value: sin(2*pi) = 0 and derivative 2*cos(2*pi) = 2

[5]:

data: -1.0717958634011433e-07, grad: 1.9999999999999885

Crank-Nicolson Summary

Neumann Boundary Conditions

When Neumann boundary conditions \(\beta_L^\prime, \beta_R^\prime\) are given instead of Dirichlet, we set \begin{align*} &-\frac{3}{2\Delta x} U_0 + \frac{4}{2\Delta x} U_1 -\frac{1}{2\Delta x} U_2 = \beta_L^\prime, \\ &\frac{3}{2\Delta x} U_m - \frac{4}{2\Delta x} U_{m-1} +\frac{1}{2\Delta x} U_{m-2} = \beta_R^\prime, \end{align*} where the left hand side are 2nd order approximation of the \(u_x\) values at both boundaries, derived from the method of undetermined coefficients. This can be computed by, for example, the Finite Difference Coefficients Calculator. Equivalently, we can write \begin{align*} U_0 &= -\frac{2\Delta x}{3}\beta_L^\prime + \frac{4}{3} U_1 - \frac{1}{3} U_2, \\ U_m &= \frac{2\Delta x}{3}\beta_R^\prime + \frac{4}{3} U_{m-1} - \frac{1}{3} U_{m-2}. \end{align*} Replacing all \(\beta_L\) and \(\beta_R\) in the above linear system by these new expressions of \(U_0\) and \(U_m\), we obtain the following linear system with Neumann BCs: \begin{align*} & \begin{pmatrix} 1+2\alpha-\frac{4}{3}\alpha & -\alpha+\frac{1}{3}\alpha&&&&\\ -\alpha & 1+2\alpha & -\alpha&&&\\ & -\alpha & 1+2\alpha & -\alpha&&\\ &&& \ddots &\\ &&& -\alpha & 1+2\alpha & -\alpha \\ &&&& -\alpha+\frac{1}{3}\alpha & 1+2\alpha-\frac{4}{3}\alpha \end{pmatrix}U^{n+1} + \begin{pmatrix} \frac{2\alpha\Delta x}{3}(\beta_L^\prime)^{n+1}\\ 0\\ 0\\ \vdots\\ 0\\ -\frac{2\alpha\Delta x}{3}(\beta_R^\prime)^{n+1}\\ \end{pmatrix} \\ &= \begin{pmatrix} 1-2\alpha +\frac{4}{3}\alpha & \alpha-\frac{1}{3}\alpha&&&&\\ \alpha & 1-2\alpha & \alpha&&&\\ & \alpha & 1-2\alpha & \alpha&&\\ &&& \ddots &\\ &&& \alpha & 1-2\alpha & \alpha \\ &&&& \alpha-\frac{1}{3}\alpha & 1-2\alpha+\frac{4}{3}\alpha \end{pmatrix}U^{n} + \begin{pmatrix} -\frac{2\alpha\Delta x}{3}(\beta_L^\prime)^{n}\\ 0\\ 0\\ \vdots\\ 0\\ \frac{2\alpha\Delta x}{3}(\beta_R^\prime)^{n}\\ \end{pmatrix}. \end{align*}

Nonlinear Term

When there is a nonlinear term in the equation, say the PDE is \(u_t = Lu + N(u)\), then the corresponding Crank-Nicolson method is \begin{align*} U^{n+1} &= U^{n} + \int_{t_n}^{t_{n+1}} \dot U\,dt\\ &= U^{n} + \int_{t_n}^{t_{n+1}} L_h U + N(U)\,dt\\ &\approx U^{n} + \Delta t\left(\frac{L_h U^{n} + N(U^{n}) + L_h U^{n+1} + N(U^{n+1})}{2}\right). \end{align*} Thus \begin{align*} \left(I - \frac{\Delta t}{2}L_h \right)U^{n+1} - \frac{\Delta t}{2} N(U^{n+1}) = \left(I + \frac{\Delta t}{2}L_h \right)U^{n} + \frac{\Delta t}{2} N(U^{n}). \end{align*} Now on the right hand side apply the 2nd order approximation (in \(t\)) \begin{align*} N(U^{n+1}) = N(U^{n}) + (U^{n+1} - U^{n})\circ N^\prime(U^n), \end{align*} where \(\circ\) denotes the element-wise product. We obtain \begin{align*} &\left(I - \frac{\Delta t}{2}L_h \right)U^{n+1} - \frac{\Delta t}{2} \left(N(U^{n}) + (U^{n+1} - U^{n})\circ N^\prime(U^n)\right) = \left(I + \frac{\Delta t}{2}L_h \right)U^{n} + \frac{\Delta t}{2} N(U^{n})\\ \implies\quad&\left(I - \frac{\Delta t}{2}L_h \right)U^{n+1} - \frac{\Delta t}{2} N^\prime(U^n)\circ U^{n+1} = \left(I + \frac{\Delta t}{2}L_h\right)U^{n} - \frac{\Delta t}{2} N^\prime(U^n)\circ U^{n} + \Delta t N(U^n)\\ \implies\quad&\left(I - \frac{\Delta t}{2}L_h - \frac{\Delta t}{2} N^\prime(U^n)\right)U^{n+1} = \left(I + \frac{\Delta t}{2}L_h - \frac{\Delta t}{2} N^\prime(U^n)\right)U^{n} + \Delta t N(U^n). \end{align*} In most cases this requires reconstruction of the matrix at each time step. Note that the above argument is not specific to finite difference method. Same argument works for spectral methods too.

Alternating-Direction Implicit Method (No Cross Term)

ADI With Cross Term

To solve \(u_t = u_{xx} + u_{yy} + u_{xy}\), first discretize in space to get the system of ODEs

where \begin{align*} \delta_x^0 &= \frac{S_x-S_x^{-1}}{2\Delta x}, \\ \delta_y^0 &= \frac{S_y-S_y^{-1}}{2\Delta y}. \end{align*} No way to split the operator into separate ones in different directions, we treat the mixed derivative fully explicitly and write \begin{align*} \left(I - \frac{\Delta t}{2}(\delta_x^+\delta_x^- + \delta_y^+\delta_y^-) \right)U^{n+1} = \left(I + \frac{\Delta t}{2}(\delta_x^+\delta_x^- + \delta_y^+\delta_y^-) + \Delta t\delta_x^0\delta_y^0\right)U^{n}. \end{align*} By splitting the opertor only on the left, we obtain \begin{align*} \left(I - \frac{\Delta t}{2}\delta_x^+\delta_x^- \right)\left(I - \frac{\Delta t}{2}\delta_y^+\delta_y^- \right)U^{n+1} = \left(I + \frac{\Delta t}{2}(\delta_x^+\delta_x^- + \delta_y^+\delta_y^-) + \Delta t\delta_x^0\delta_y^0\right)U^{n}. \end{align*} A variant of this scheme is the Douglas-Rachford scheme \begin{align*} &\left(I - \frac{\Delta t}{2}\delta_x^+\delta_x^- \right)V^n = \left(I + \frac{\Delta t}{2}\delta_x^+\delta_x^- + \Delta t\delta_y^+\delta_y^- + \Delta t\delta_x^0\delta_y^0\right)U^{n}, \\ &\left(I - \frac{\Delta t}{2}\delta_y^+\delta_y^- \right)U^{n+1} = V^n - \frac{\Delta t}{2}\delta_y^+\delta_y^- U^n. \end{align*} Since the cross term is not integrated with the trapezoidal rule, the convergence order in time of the Douglas-Rachford reduces to 1. To recover 2nd order convergence in time, apply a predictor-corrector scheme:

Predictor: \begin{align*} \left(I - \frac{\Delta t}{2}\delta_x^+\delta_x^- \right)V_1^{n} &= \left(I + \frac{\Delta t}{2}\delta_x^+\delta_x^- + \Delta t\delta_y^+\delta_y^- + \Delta t\delta_x^0\delta_y^0\right)U^{n}, \\ \left(I - \frac{\Delta t}{2}\delta_y^+\delta_y^- \right)V_2^{n} &= V_1^n - \frac{\Delta t}{2}\delta_y^+\delta_y^- U^n. \end{align*}

Corrector: \begin{align*} &\left(I - \frac{\Delta t}{2}\delta_x^+\delta_x^- \right)V_3^{n} = \left(I + \frac{\Delta t}{2}\delta_x^+\delta_x^- + \Delta t \delta_y^+\delta_y^- + \frac{\Delta t}{2}\delta_x^0\delta_y^0\right)U^{n} + \frac{\Delta t}{2} V_2^{n}, \\ &\left(I - \frac{\Delta t}{2}\delta_y^+\delta_y^- \right)U^{n+1} = V_3^n - \frac{\Delta t}{2}\delta_y^+\delta_y^- U^n. \end{align*}

Here the Douglas-Rachford scheme is first applied and the result \(V_2^{n}\) is a predictor of the solution at time \(t_{n+1}\), to be corrected. This scheme has 2nd order convergence both in time and space.

Spectral Method Summary (Nodal Continuous Galerkin)

To solve \(u_t = u_{xx}\) in \(x\in[-1, 1]\), first write it in weak form and integrate by part in \(x\): \begin{align*} \int_{-1}^1 u_t(t, x)\phi(x)\,dx &= \int_{-1}^{1} u_{xx}(t, x)\phi(x)\,dx\\ &= u_{x}\phi(x)\Big|_{-1}^1 - \int_{-1}^1 u_{x}\phi^\prime(x)\,dx\\ &= - \int_{-1}^1 u_{x}\phi^\prime(x)\,dx, \end{align*} where the last equation holds as long as we choose a function \(\phi(x)\) that vanishes at the boundaries. Replacing all functions by Lagrange interpolating polynomials and integrals by Gauss-Lobatto quadratures \begin{align*} u(t, x) &\approx \sum_{p=0}^N U_p(t)\ell_p(x),\\ \phi(x) &\approx \sum_{i=0}^N \phi_i\ell_i(x),\\ \int_{-1}^1 f(x)\,dx &\approx \sum_{n=0}^N f(x_n)w_n, \end{align*} we get \begin{align*} \sum_{p=0}^N\sum_{i=0}^N\sum_{n=0}^N \dot U_p(t)\ell_p(x_n)\phi_i\ell_i(x_n)w_n =& -\sum_{p=0}^N\sum_{i=0}^N\sum_{n=0}^N U_p(t)\ell_p^\prime(x_n)\phi_i\ell_i^\prime(x_n)w_n. \end{align*} Note that doing so we have introduced an error in space and the error is of order \(O\left(C^{-N}\right)\) as the functions are smooth. There are many zero terms in the above equation as the Lagrange basis polynomials have the property \begin{align*} \ell_p(x_n) = \begin{cases} 1 &\mbox{ if }p=n\\ 0 &\mbox{ if }p\ne n \end{cases}. \end{align*} Get rid of the zero terms to get \begin{align*} \sum_{i=0}^N \dot U_i(t)\phi_iw_i =& -\sum_{p=0}^N\sum_{i=0}^N\sum_{n=0}^N U_p(t)\ell_p^\prime(x_n)\phi_i\ell_i^\prime(x_n)w_n\\ =& -\sum_{p=0}^N\sum_{i=0}^N\sum_{n=0}^N U_p(t)D_{np}\phi_iD_{ni}w_n, \end{align*} where \(D_{ij} = \ell_j^\prime(x_i)\). As this holds for arbitrary \(\phi_i\)’s, the coefficients of \(\phi_i\) on both sides should equal: \begin{align*} \dot U_i(t) w_i =& -\sum_{p=0}^N\sum_{n=0}^N U_p(t)D_{np}D_{ni}w_n\qquad \forall i=1, 2, \ldots, N-1. \end{align*} Next we write the equation in matrix form using the identity \((Ax)_i = \sum_j A_{ij}x_j\). We obtain \begin{align*} W\dot{\vec{U}} = -D^TWD\vec U, \end{align*} where \begin{align*} &\vec U = \begin{pmatrix} U_0(t)\\ U_1(t)\\ U_2(t)\\ \vdots\\ U_N(t) \end{pmatrix}, W = \begin{pmatrix} w_0 & & & & 0 \\ & w_1 & & & \\ & & w_2 & & \\ & & & \ddots & \\ 0 & & & & w_N \end{pmatrix}, \\\\ &D = \begin{pmatrix} D_{00} & D_{01} & D_{02} & \cdots & D_{0N} \\ D_{10} & D_{11} & D_{12} & \cdots & D_{1N} \\ D_{20} & D_{21} & D_{22} & \cdots & D_{2N} \\ \vdots & \vdots & \vdots & \ddots & \vdots \\ D_{N0} & D_{N1} & D_{N2} & \cdots & D_{NN} \end{pmatrix} = \begin{pmatrix} \ell_0^\prime(\xi_0) & \ell_1^\prime(\xi_0) & \ell_2^\prime(\xi_0) & \cdots & \ell_N^\prime(\xi_0) \\ \ell_0^\prime(\xi_1) & \ell_1^\prime(\xi_1) & \ell_2^\prime(\xi_1) & \cdots & \ell_N^\prime(\xi_1) \\ \ell_0^\prime(\xi_2) & \ell_1^\prime(\xi_2) & \ell_2^\prime(\xi_2) & \cdots & \ell_N^\prime(\xi_2) \\ \vdots & \vdots & \vdots & \ddots & \vdots \\ \ell_0^\prime(\xi_N) & \ell_1^\prime(\xi_N) & \ell_2^\prime(\xi_N) & \cdots & \ell_N^\prime(\xi_N) \end{pmatrix}, \end{align*} or equivalently \begin{align*} \dot{\vec{U}} = -W^{-1}D^TWD\vec U = L\vec U, \end{align*} where \(L = -W^{-1}D^TWD\). Now discretize \(t\) and apply the trapezoidal rule, \begin{align*} \vec U(t_{n+1}) &= \vec U(t_n) + \int_{t_n}^{t_{n+1}} \dot{\vec U}(t)\,dt\\ &= \vec U(t_n) + \int_{t_n}^{t_{n+1}} L\vec U(t)\,dt\\ &\approx \vec U(t_n) + \frac{\Delta t L}{2}\left(\vec U(t_n) + \vec U(t_{n+1}) \right). \end{align*} Rearrange the terms to obtain the linear system we need to solve: \begin{align*} \left(I - \frac{\Delta t}{2}L\right)\vec U(t_{n+1}) = \left(I + \frac{\Delta t}{2}L\right)\vec U(t_n). \end{align*}

Spectral Method in Multidimensions (Nodal Continuous Galerkin)

The goal here is to solve \(u_t = \mathcal L u(\vec x)\) on \(\vec x\in\Omega = [-1, 1]\times[-1, 1]\). For simplicity, think of \(\mathcal L\) as for example the 2D Laplacian \(\mathcal L u(x, y) = u_{xx} + u_{yy}\), but the below argument holds for any operators in the form \begin{align*} \mathcal L = a\frac{\partial^2}{\partial x^2} + b\frac{\partial^2}{\partial x\partial y} + c\frac{\partial^2}{\partial y^2} + d\frac{\partial}{\partial x} + e\frac{\partial}{\partial y} + f. \end{align*} First write the PDE in weak form: \begin{align*} \int_\Omega u_t(t, \vec x)\phi(\vec x)\,d\vec x &= \int_\Omega \mathcal L u(t, \vec x)\phi(\vec x)\,d\vec x. \end{align*} Now replace all functions by Lagrange interpolating polynomials and integrals by Gauss-Lobatto quadratures \begin{align*} u(t, \vec x) &\approx \sum_{\mathbf p} U_\mathbf p(t)\ell_\mathbf p(\vec x),\\ \phi(\vec x) &\approx \sum_{\mathbf i} \phi_\mathbf i\ell_\mathbf i(\vec x),\\ \int_\Omega f(\vec x)\,d\vec x &\approx \sum_{\mathbf n} f(\vec x_\mathbf n)w_\mathbf n, \end{align*} where the boldface indices are in multidimensions, for example \(\mathbf i\) can be \((0, 0), (0, 1), (1, 1), \ldots\). We obtain \begin{align*} \sum_{\mathbf p}\sum_{\mathbf i}\sum_{\mathbf n} \dot U_\mathbf p(t)\ell_\mathbf p(\vec x_\mathbf n)\phi_\mathbf i\ell_\mathbf i(\vec x_\mathbf n)w_\mathbf n =& \sum_{\mathbf p}\sum_{\mathbf i}\sum_{\mathbf n} U_\mathbf p(t)\mathcal L\ell_\mathbf p(\vec x_\mathbf n)\phi_\mathbf i\ell_\mathbf i(\vec x_\mathbf n)w_\mathbf n. \end{align*} Note that doing so we have introduced an error in space and the error is of order \(O\left(C^{-N}\right)\) if the functions are analytic, where \(N\) is total number of nodes in one dimension. There are many zero terms in the above equation as the Lagrange basis polynomials have the property \begin{align*} \ell_\mathbf p(\vec x_\mathbf n) = \begin{cases} 1 &\mbox{ if }\mathbf p=\mathbf n\\ 0 &\mbox{ if }\mathbf p\ne \mathbf n \end{cases}. \end{align*} Get rid of the zero terms to get \begin{align*} \sum_{\mathbf i} \dot U_\mathbf i(t)\phi_\mathbf iw_\mathbf i =& \sum_{\mathbf p}\sum_{\mathbf i} U_\mathbf p(t)\mathcal L\ell_\mathbf p(\vec x_\mathbf i)\phi_\mathbf iw_\mathbf i\\ =& \sum_{\mathbf p}\sum_{\mathbf i} U_\mathbf p(t)L_{\mathbf i\mathbf p}\phi_\mathbf iw_\mathbf i, \end{align*} where \(L_{\mathbf i\mathbf j} = \mathcal L\ell_\mathbf j(\vec x_\mathbf i)\). As this holds for arbitrary \(\phi_\mathbf i\)’s, the coefficients of \(\phi_\mathbf iw_\mathbf i\) on both sides should equal: \begin{align*} \dot U_\mathbf i(t) =& \sum_{\mathbf p}U_\mathbf p(t)L_{\mathbf i\mathbf p}\qquad \forall \mathbf i. \end{align*} Next we write the equation in matrix form using the identity \((Ax)_\mathbf i = \sum_{\mathbf j} A_{\mathbf i\mathbf j}x_\mathbf j\). We obtain a clean \begin{align*} \dot{\vec{U}} = L\vec U. \end{align*} Now discretize \(t\) and apply the trapezoidal rule, \begin{align*} \vec U(t_{n+1}) &= \vec U(t_n) + \int_{t_\mathbf n}^{t_{n+1}} \dot{\vec U}(t)\,dt\\ &= \vec U(t_n) + \int_{t_n}^{t_{n+1}} L\vec U(t)\,dt\\ &\approx \vec U(t_n) + \frac{\Delta t L}{2}\left(\vec U(t_n) + \vec U(t_{n+1}) \right). \end{align*} Rearrange the terms to obtain the linear system we need to solve: \begin{align*} \left(I - \frac{\Delta t}{2}L\right)\vec U(t_{n+1}) = \left(I + \frac{\Delta t}{2}L\right)\vec U(t_n). \end{align*}

Dirichlet Boundary Conditions

Given Dirichlet boundary conditions, in the system of ODEs \begin{align*} \dot U_\mathbf i(t) =& \sum_{\mathbf p}U_\mathbf p(t)L_{\mathbf i\mathbf p}\qquad \forall \mathbf i, \end{align*} \(U_\mathbf i(t)\) values at the boundary are known so no need to solve ODEs for those. Denote by \(\mathbf i_{\text{int}}\) and \(\mathbf p_{\text{int}}\) indices for interior points of \(\Omega\), and denote by \(\mathbf i_{\text{bdy}}\) and \(\mathbf p_{\text{bdy}}\) indices for points at the boundary. We are only interested in \begin{align*} \dot U_{\mathbf i_{\text{int}}}(t) =& \sum_{\mathbf p}U_\mathbf p(t)L_{\mathbf i_{\text{int}}\mathbf p}\\ =& \sum_{\mathbf p_{\text{int}}}U_{\mathbf p_{\text{int}}}(t)L_{\mathbf i_{\text{int}}\mathbf p_{\text{int}}} + \sum_{\mathbf p_{\text{bdy}}}U_{\mathbf p_{\text{bdy}}}(t)L_{\mathbf i_{\text{int}}\mathbf p_{\text{bdy}}}, \end{align*} where the 2nd term in the last equation is simply a known scalar as the \(U_{\mathbf p_{\text{bdy}}}(t)\) values are given. In matrix form, the system of ODEs is \begin{align*} \dot{\vec U}_{\text{int}} =& L_{\text{int}} \vec U_{\text{int}} + L_{\text{int, bdy}} \vec U_{\text{bdy}}, \end{align*} where \({\vec U}_{\text{int}}\) is a vector of all \(U_{\mathbf i_{\text{int}}}(t)\) at interior points, \({\vec U}_{\text{bdy}}\) a vector of all \(U_{\mathbf i_{\text{bdy}}}(t)\) at the boundary, and \(L_{\text{int, bdy}}\) is a (tall) matrix of all \(L_{{\mathbf i_{\text{int}}}{\mathbf p_{\text{bdy}}}} = \mathcal L\ell_{\mathbf p_{\text{bdy}}}(\vec x_{\mathbf i_{\text{int}}})\), that’s the Laplacian of all boundary Lagrange basis functions at interior points.

Sparse Grid

[1]:

# sparse grid

from pandas import DataFrame, Series

from numpy import cos, pi

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

def stat(q=6):

d = 2 # below code assumes 2D; d values other than 2 doesn't make sense

### chebyshev spectral method

sem = DataFrame(sum([[(cos(i*pi/2**n), cos(j*pi/2**m)) for i in np.arange(2**n+1) for j in np.arange(2**m+1)]

for m in range(1, q) for n in range(1, q) if d <= m+n <= q], []), columns=['x', 'y']).drop_duplicates()

### finite difference

fdm = DataFrame(sum([[(i/2**(n-1)-1, j/2**(m-1)-1) for i in np.arange(2**n+1) for j in np.arange(2**m+1)]

for m in range(1, q) for n in range(1, q) if d <= m+n <= q], []), columns=['x', 'y']).drop_duplicates()

if q==7:

fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(14, 7))

sem.plot(kind='scatter', x='x', y='y', ax=ax1)

ax1.set_title(f'Chebyshev-Gauss-Lobatto Points (q = {q})')

fdm.plot(kind='scatter', x='x', y='y', ax=ax2)

ax2.set_title(f'Uniform Grid (q = {q})')

interior_pts = sem[(sem['x'] != -1) & (sem['x'] != 1) & (sem['y'] != -1) & (sem['y'] != 1)]

return Series({

'q': q,

'd': d,

'number of grid points on one boundary': (2**(q-1)+1),

'number of full grid points': (2**(q-1)+1)**2,

'number of sparse grid points': sem.shape[0],

'number of full grid interior points': (2**(q-1)-1)**2,

'number of sparse grid interior points': interior_pts.shape[0],

'ratio number of interior points (sparse/full) x 100 (in %)': int((interior_pts.shape[0]/(2**(q-1)-1)**2)*100)

})

pd.options.display.float_format = '{:,d}'.format # this is for floats, but if you need a temporary global integer display for floats.

DataFrame([stat(q) for q in range(2, 11)]).set_index('q').T

[1]:

| q | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

|---|---|---|---|---|---|---|---|---|---|

| d | 2 | 2 | 2 | 2 | 2 | 2 | 2 | 2 | 2 |

| number of grid points on one boundary | 3 | 5 | 9 | 17 | 33 | 65 | 129 | 257 | 513 |

| number of full grid points | 9 | 25 | 81 | 289 | 1089 | 4225 | 16641 | 66049 | 263169 |

| number of sparse grid points | 9 | 21 | 49 | 113 | 257 | 577 | 1281 | 2817 | 6145 |

| number of full grid interior points | 1 | 9 | 49 | 225 | 961 | 3969 | 16129 | 65025 | 261121 |

| number of sparse grid interior points | 1 | 5 | 17 | 49 | 129 | 321 | 769 | 1793 | 4097 |

| ratio number of interior points (sparse/full) x 100 (in %) | 100 | 55 | 34 | 21 | 13 | 8 | 4 | 2 | 1 |

PDE on GPU Grid

有了 cuPyNumeric,應該不管幾維都用 numpy 寫 CN + GMRES,開發起來快,跑的也快

Thomas algorithm 只能 sequential 跑,沒辦法用 GPU 加速

GMRES 可以平行計算,雖然計算量較大但在用 GPU 加速之後當矩陣很大的時候(\(N\) 從 1,000 到 10,000)會比 Thomas algorithm 快

\(N<1000\) 時 CPU 上的 Thomas algorithm 會比較快

CPU-GPU data transfer 也有 overhead,\(N\) 太小不划算

GPU 計算 32-bit float 比 64-bit double 快很多

Linear System Solvers:

如果矩陣是 positive definite(通常不是)就用 CG,保證最快 + 保證收斂(數學上)

BiCGSTAB 通常比 GMRES 快的多但不保證收斂

GMRES 保證收斂(數學上)但需要存下疊代過程中每一步的向量,對記憶體要求高

目前(2025/8)legate_sparse 和 cupyx.scipy.sparse 裡都有 GMRES,都沒有 BiCGSTAB

只有 scipy.sparse.linalg 裡有 BiCGSTAB

Initial Guess for Linear Systems

如果發現 Forward Euler 提供的初始猜測不足以顯著減少迭代次數,可以用更高階的顯式方法(例如二階的 Runge-Kutta,Heun’s method)來計算初始猜測。然而,對於許多問題,單純的 Forward Euler 已經足夠

Forward Euler 誤差 \(O(\Delta t)\),CN 誤差 \(O(\Delta t^2)\),如果 \(\Delta t\) 很大,Forward Euler 會是一個很差的初值

可以平行計算的 preconditioner:

Diagonal (Jacobi)

Block Jacobi

Block Gauss-Seidel

Block SOR

Sparse Approximate Inverse Preconditioners

Polynomial Preconditioners

\(M^{-1} = P(A) = c_0I+c_1A + c_2A^2 + \cdots + c_kA^k\)

如果不考慮開發成本,效能最高的解決方案是結合 Parallel Cyclic Reduction (PCR) 的並行性與 Thomas algorithm 的效率,或者將大問題分解成小批次,利用 GPU 的批處理能力

Double-Precision Floating-Point Format

IEEE 754 standard:

\(E\) 是 biased exponent,從 0 到 2047 之間的一個整數

Exponent \(E - 1023\) 是從 -1023 到 1024 之間的一個整數

當 sign 和 exponent 都是零,浮點數是 \((1.b_{51}b_{50}...b_{0})_{2} \in [1, 2)\)

若 exponent 為 1,把一樣多的數(\(2^{52}\) 個)塞到 \([2, 4)\) 之間但 gap 放大兩倍

若 exponent 為 2,再把一樣多的數塞到 \([4, 8)\) 之間,gap 再放大兩倍,以此類推

若 exponent 為 -1,把一樣多的數塞到 \([0.5, 1)\) 之間,gap 再縮小成一半,以此類推

特殊值

類型 |

Sign Bit |

Exponent (11 bits) |

Fraction (52 bits) |

說明 |

|---|---|---|---|---|

+Infinity |

0 |

|

|

正無窮 |

-Infinity |

1 |

|

|

負無窮 |

Quiet NaN |

任意 |

|

|

不中斷運算的「無效數值」 |

Signaling NaN |

任意 |

|

|

可能觸發錯誤的 NaN |

+0 |

0 |

|

|

正零 |

-0 |

1 |

|

|

負零 |

Example: \(X\) and \(Y\) Are Both Normal but \(X+Y\) Is Not

Consider

\(X\sim N(0, 1)\),

\(S \perp\!\!\!\perp X\) a random sign with \(P(S=1) = P(S=-1) = 1/2\), and

\(Y=SX\).

We will have \(Y\sim N(0, 1)\) (similar to Gaussian mixture), but for the sum \(X+Y\) we have \begin{align*} X+Y = \begin{cases} 2X &\quad\text{ if } S=1\\ 0 &\quad\text{ if } S=-1 \end{cases}. \end{align*} So we have 1/2 of probability mass concentrated at 0 in which case \(X+Y\) cannot be normal.

The joint pdf of \((X, Y)\) is an X shaped fin on the \(xy\) plane.

Copula

Definition and Usage

A \(d\)-dimensional copula is a CDF defined on \([0, 1]^d\) such that all marginal distributions are Uniform(0, 1)

Sklar’s theorem: Under regularity conditions, any multivariate CDF can be uniquely written in terms of its marginal CDFs and some copula

Gauss copula in 2D is defined as \begin{align*} C_{\rho}(u, v) = \Phi_{\rho}(\Phi^{-1}(u), \Phi^{-1}(v)), \end{align*} where \(\Phi\) is the 1D standard normal CDF and \(\Phi_{\rho}\) is the bivariate normal CDF with covariance matrix \begin{align*} \begin{bmatrix} 1 & \rho \\ \rho & 1 \end{bmatrix} \end{align*}

The copula density is \begin{align*} c_\rho(u, v) = \frac{\partial C_{\rho}}{\partial v\partial v}(u, v) = \frac{\phi_{\rho}(\Phi^{-1}(u), \Phi^{-1}(v))}{\phi(\Phi^{-1}(u))\phi(\Phi^{-1}(v))}, \end{align*} where \(\phi\) is the 1D standard normal PDF and \(\phi_{\rho}\) is the bivariate normal PDF with the same covariance matrix

The bivariate CDF \begin{align*} C_{\rho}(F_x(x), F_y(y)) \end{align*} has marginal CDFs \(F_x, F_y\) and Gauss copula correlation \(\rho\), and the corresponding PDF is \begin{align*} c_{\rho}(F_x(x), F_y(y))f_X(x)f_Y(y) \end{align*}

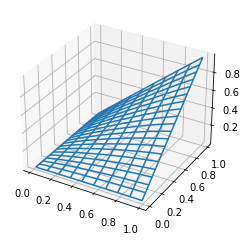

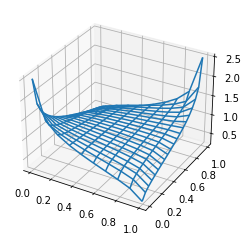

[10]:

import matplotlib.pyplot as plt

import numpy as np

from pandas import DataFrame

from scipy.stats import norm, multivariate_normal

def C(u, v, rho):

'''Bivariate Gauss copula'''

return multivariate_normal.cdf([norm.ppf(u), norm.ppf(v)], cov=[[1.0, rho], [rho, 1.0]])

def c(u, v, rho):

'''Bivariate Gauss copula density'''

return multivariate_normal.pdf([norm.ppf(u), norm.ppf(v)], cov=[[1.0, rho], [rho, 1.0]])/(norm.pdf(norm.ppf(u))*norm.pdf(norm.ppf(v)))

def plot_surf(f, x, y, fillna=0):

Z = np.array([[f(xi, yi) for xi in x] for yi in y])

Z[np.isnan(Z)] = fillna

X = np.array([x for _ in y])

Y = np.array([y for _ in x]).T

fig = plt.figure()

ax = plt.axes(projection='3d')

ax.plot_wireframe(X, Y, Z)

rho = 0.2

x = np.linspace(0.01, 0.99, 10)

y = np.linspace(0.01, 0.99, 20)

plot_surf(lambda x, y: C(x, y, rho), x, y)

plot_surf(lambda x, y: c(x, y, rho), x, y, fillna=None)

[7]:

from ipywidgets import interact

@interact(rho=(-0.9, 0.99, 0.1))

def f(rho=0.2):

x = np.linspace(0.01, 0.99, 10)

y = np.linspace(0.01, 0.99, 20)

plot_surf(lambda x, y: C(x, y, rho), x, y)

plot_surf(lambda x, y: c(x, y, rho), x, y, fillna=None)

Simulation

To simulate from Gauss copula:

generate normal random variables with the given covariance matrix

plug every number into standard normal CDF so that the marginal distributions are uniform

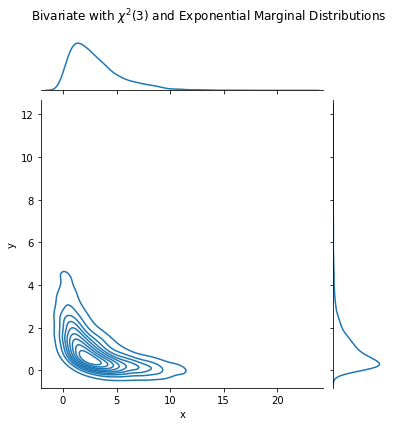

To simulate from a joint distribution such that the marginal distribution of \(x, y\) are \(\chi^2\) and exponential, respectively:

generate Gauss copula random numbers

plug \(x\) values into \(\chi^2\) inverse CDF, and \(y\) values into exponential inverse CDF

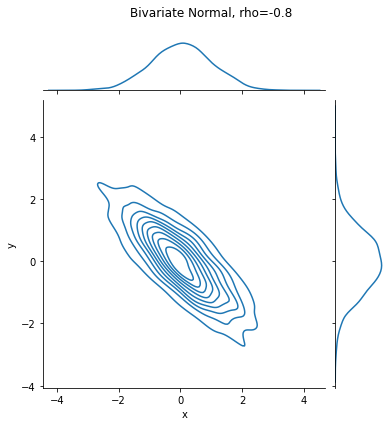

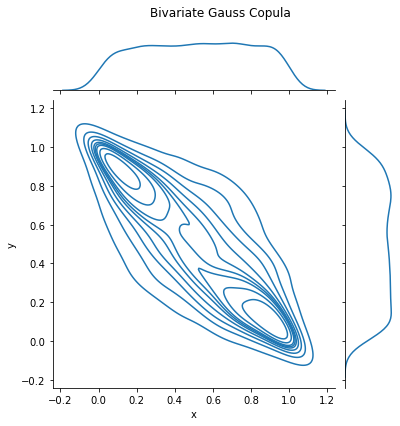

[13]:

from scipy.stats import norm, multivariate_normal, chi2, expon

from pandas import DataFrame

import matplotlib.pyplot as plt

import numpy as np

import seaborn as sns

def plot_data(data, title):

'''jointplot a DataFrame with 'x' and 'y' columns'''

p = sns.jointplot(x='x', y='y', kind='kde', data=data)

p.fig.suptitle(title)

p.fig.subplots_adjust(top=0.9, right=0.9)

rho = -0.8

n = 2000

np.random.seed(0)

data = DataFrame(multivariate_normal(cov=[[1.0, rho], [rho, 1.0]]).rvs(n), columns=['x', 'y'])

plot_data(data=data, title='Bivariate Normal, rho=-0.8')

data = data.applymap(norm.cdf)

plot_data(data=data, title='Bivariate Gauss Copula')

data['x'] = data['x'].map(chi2(df=3).ppf)

data['y'] = data['y'].map(expon.ppf)

plot_data(data=data, title='Bivariate with $\chi^2(3)$ and Exponential Marginal Distributions')

Notes on LMM

Let \(q(t)\) be the index such that \(T_{q(t)-1} \le t < T_{q(t)}\). Then the dynamics of the forward rate \(L_n(t) = L(t, T_n, T_{n+1})\) in the spot measure \(Q^B\) is \begin{align*} dL_n(t) = \sigma_n(t)^T\left(\sum_{j=q(t)}^n\frac{\tau_j\sigma_j(t)}{1+\tau_j L_j(t)} dt + dW^B(t)\right). \end{align*} This is the discrete version of the HJM forward rate dynamics \begin{align*} df(t, T) = \sigma(t, T)^T \left(\Sigma(t, T)dt + d \widetilde W_t\right). \end{align*} Adding stochastic volatility, the model is \begin{align*} dz(t) &= \theta(1 - z(t))dt + \eta\sqrt{z(t)}dZ^B(t), \\ dL_n(t) &= \sqrt{z(t)}\phi(L_n(t))\lambda_n(t)^T\left(\sqrt{z(t)}\mu_n(t) dt + dW^B(t)\right), \\ \mu_n(t) &= \sum_{j=q(t)}^n\frac{\tau_j\phi(L_j(t))\lambda_j(t)}{1+\tau_j L_j(t)}. \end{align*}

LMM SV With Non-zero Correlation

Consider one factor normal LMM with SV \begin{align*} &dL_n(t) = \sigma_n \sqrt{z(t)}dW^{n+1}(t) = \sigma_n\sqrt{z(t)}\left(\sum_{j=q(t)}^n\frac{\tau_j \sigma_j\sqrt{z(t)}}{1+\tau_jL_j(t)}dt + dW^B(t)\right), \\ &dz(t) = \theta(1-z(t))\,dt + \eta\sqrt{z(t)}\,dZ^B(t), \\ &dZ^B(t)\,dW^B(t) = \rho\,dt. \end{align*} One can write \begin{align*} dZ^B(t) = \rho\,dW^B(t) + \sqrt{1-\rho^2}\,d\widetilde W(t) \end{align*} for some independent Brownian motion \(\widetilde W(t)\). Thus \begin{align*} dz(t) &= \theta(1-z(t))\,dt + \eta\sqrt{z(t)}\,dZ^B(t)\\ &= \theta(1-z(t))\,dt + \eta\sqrt{z(t)}\left(\rho\,dW^B(t) + \sqrt{1-\rho^2}\,d\widetilde W(t)\right)\\ &= \theta(1-z(t))\,dt + \eta\sqrt{z(t)}\left(\rho\left(-\sum_{j=q(t)}^n\frac{\tau_j \sigma_j\sqrt{z(t)}}{1+\tau_jL_j(t)}dt + dW^{n+1}(t)\right) + \sqrt{1-\rho^2}\,d\widetilde W(t)\right)\\ &= \theta(1-\alpha(t)z(t))\,dt + \eta\sqrt{z(t)}\left(\rho\,dW^{n+1}(t) + \sqrt{1-\rho^2}\,d\widetilde W(t)\right)\\ &= \theta(1-\alpha(t)z(t))\,dt + \eta\sqrt{z(t)}\,dZ^{n+1}(t), \end{align*} where \(dZ^{n+1}(t)\,dW^{n+1}(t) = \rho\,dt\) and \begin{align*} \alpha(t) = 1+\frac{\eta\rho}{\theta}\sum_{j=q(t)}^n\frac{\tau_j \sigma_j}{1+\tau_jL_j(t)}. \end{align*}

LMM Related Questions

What’s the LIBOR 3M forward rate?

Forward rate is a martingale under what measure? What’s its corresponding numeraire?

What about futures rate? What’s its corresponding numeraire?

\(L_n\) dynamics under \(T_n\) forward measure? (1 term in the BGM drift term)

Describe PCA for dimension reduction in BGM. What data do you use?

Which one in the picture is the 1st PC, which one is 2nd?

What is skew? How does BGM capture skew?

What’s that you calibrate in BGM?

Where is today’s volatility hump in BGM vol grid?

What are your calibration instruments? How do you price swaptions? In a high level, describe how the approximation is derived

Describe how to price a vanilla swaption using a calibrated BGM model with MC

What’s the Longstaff-Schwartz algorithm?

What’s SOFR

3M SOFR futures Sept 2022 contract – term rate from what window? When is the last trade date? When is the fixing date?

How to modify BGM volatility to model SOFR index?

How to modify BGM measure to model SOFR index? (Extended bond price: buy \(T\)-bond and reinvest in MMA after \(T\))

How does SABR handle negative rates? What’s a reasonable way to determine shift?

SABR model: how does each parameter control the shape of the implied vol?

HW2F Summary

Let \begin{align*} h(t) &= \begin{bmatrix} e^{-\kappa_1 t}\\ e^{-\kappa_2 t} \end{bmatrix}_{2\times 1}, \\ g(t) &= \begin{bmatrix} \sigma_1\sqrt{1-\rho^2} e^{\kappa_1 t} & 0\\ \sigma_1\rho e^{\kappa_1 t} & \sigma_2 e^{\kappa_2 t} \end{bmatrix}_{2\times 2}. \end{align*} The HJM forward rate vol is \begin{align*} \sigma(t, T) = g(t)h(T) = \begin{bmatrix} \sigma_1\sqrt{1-\rho^2} e^{-\kappa_1 (T-t)} \\ \sigma_1\rho e^{-\kappa_1 (T-t)} + \sigma_2 e^{-\kappa_2 (T-t)} \end{bmatrix}_{2\times 1}, \end{align*} or, if allowing a correlation \(\rho\) between the two Brownian motions in the forward rate process, \begin{align*} \sigma^*(t, T) = \begin{bmatrix} \sigma_1 e^{-\kappa_1 (T-t)} \\ \sigma_2 e^{-\kappa_2 (T-t)} \end{bmatrix}_{2\times 1}. \end{align*}

Let \(H(t) = \operatorname{diag}(h(t))\) and \begin{align*} \sigma_x &= g(t)H(t) = \begin{bmatrix} \sigma_1\sqrt{1-\rho^2} & 0\\ \sigma_1\rho & \sigma_2 \end{bmatrix}_{2\times 2}, \\ \sigma_x^* &= \begin{bmatrix} \sigma_1 & 0\\ 0 & \sigma_2 \end{bmatrix}_{2\times 2}. \end{align*}

Let \begin{align*} \kappa &= \begin{bmatrix} \kappa_1 & 0\\ 0 & \kappa_2 \end{bmatrix}_{2\times 2}. \end{align*}

Then the short rate process is \(r(t) = f(0, t) + x_1(t) + x_2(t) = f(0, t) + x(t)\mathbf 1\), where \(x(0) = y(0) = 0\), \begin{align*} \begin{cases} dx(t) = (y(t)\mathbf 1 - \kappa x(t))dt + \sigma_x^T dW(t)\\ dy(t) = (\sigma_x^T\sigma_x - \kappa y(t) - y(t)\kappa) dt \\ dW_1(t)dW_2(t) = 0 \end{cases}, \end{align*} and the covariance matrix is \begin{align*} \sigma_x^T\sigma_x = \begin{bmatrix} \sigma_1^2 & \rho\sigma_1\sigma_2 \\ \rho\sigma_1\sigma_2 & \sigma_2^2 \end{bmatrix}_{2\times 2}. \end{align*} The ODE of \(y(t)\) can be solved explicitly to obtain \begin{align*} y(t) &= H(t)\left(\int_0^t g(s)^Tg(s)\,ds\right)H(t)\\ &= \begin{bmatrix} \frac{\sigma_1^2\left(1-e^{-2\kappa_1 t}\right)}{2\kappa_1} & \frac{\rho\sigma_1\sigma_2\left(1-e^{-(\kappa_1 + \kappa_2) t}\right)}{\kappa_1 + \kappa_2}\\ \frac{\rho\sigma_1\sigma_2\left(1-e^{-(\kappa_1 + \kappa_2) t}\right)}{\kappa_1 + \kappa_2} & \frac{\sigma_2^2\left(1-e^{-2\kappa_2 t}\right)}{2\kappa_2} \end{bmatrix}_{2\times 2}. \end{align*} Alternatively, one can write \begin{align*} \begin{cases} dx(t) = (y(t)\mathbf 1 - \kappa x(t))dt + \sigma^*_x dW^*(t) \\ dW_1^*(t)dW_2^*(t) = \rho dt \end{cases}, \end{align*} or more explicitly, \begin{align*} \begin{cases} dx_1(t) = \left(\frac{\sigma_1^2\left(1-e^{-2\kappa_1 t}\right)}{2\kappa_1} + \frac{\rho\sigma_1\sigma_2\left(1-e^{-(\kappa_1 + \kappa_2) t}\right)}{\kappa_1 + \kappa_2} - \kappa_1 x_1(t)\right)dt + \sigma_1 dW^*_1(t) \\ dx_2(t) = \left(\frac{\sigma_2^2\left(1-e^{-2\kappa_2 t}\right)}{2\kappa_2} + \frac{\rho\sigma_1\sigma_2\left(1-e^{-(\kappa_1 + \kappa_2) t}\right)}{\kappa_1 + \kappa_2} - \kappa_2 x_2(t)\right)dt + \sigma_2 dW^*_2(t) \\ dW_1^*(t)dW_2^*(t) = \rho dt \end{cases}. \end{align*}

Let \begin{align*} M(t, T) &= H(T)H(t)^{-1}\mathbf 1 = \begin{bmatrix} e^{-\kappa_1(T-t)}\\ e^{-\kappa_2(T-t)} \end{bmatrix}_{2\times 1}, \\ G(t, T) &= \int_t^TM(t, u)\,du = \begin{bmatrix} \frac{1-e^{-\kappa_1(T-t)}}{\kappa_1}\\ \frac{1-e^{-\kappa_2(T-t)}}{\kappa_2} \end{bmatrix}_{2\times 1}. \end{align*} Then the forward rate process and the zero-coupon bond price are \begin{align*} f(t, T) &= f(0, T) + M(t, T)^T(x(t) + y(t)G(t, T)), \\ P(t, T) &=\frac{P(0, T)}{P(0, t)}\exp\left(-G(t, T)^Tx(t) - \frac12G(t, T)^Ty(t)G(t, T)\right), \end{align*} respectively. Note that since \(G\) and \(M\) are both functions of \(T-t\), the dynamics of \(f(t, T)\) and \(P(t, T)\) are stationary.

The risk-neutral process of \(P(t, T)\) is log-normal \begin{align*} \frac{dP(t, T)}{P(t, T)} &= r(t)dt - (\sigma_x G(t, T))^T dW(t)\\ &= r(t)dt - (\sigma^*_x G(t, T))^T dW^*(t). \end{align*} That is, the HJM bond price vol is \(\Sigma(t, T) = \sigma_x G(t, T)\), or \begin{align*} \Sigma^*(t, T) = \sigma^*_x G(t, T) = \begin{bmatrix} \frac{\sigma_1}{\kappa_1}\left(1-e^{-\kappa_1(T-t)}\right)\\ \frac{\sigma_2}{\kappa_2}\left(1-e^{-\kappa_2(T-t)}\right) \end{bmatrix}_{2\times 1} \end{align*} if allowing a correlation \(\rho\) between the two Brownian motions in the process.

HW2F Summary New Notation

The notation here is more intuitive than Leif Andersen. Let \begin{align*} h(t) &= \begin{bmatrix} e^{-\kappa_1 t}\\ e^{-\kappa_2 t} \end{bmatrix}_{2\times 1}, \\ H(t) &= \operatorname{diag}(h(t)) = \begin{bmatrix} e^{-\kappa_1 t} & 0\\ 0 & e^{-\kappa_2 t} \end{bmatrix}_{2\times 2}, \\ \sigma_x^* &= \begin{bmatrix} \sigma_1 & 0\\ 0 & \sigma_2 \end{bmatrix}_{2\times 2}, \\ R &= \begin{bmatrix} 1 & \rho\\ \rho & 1 \end{bmatrix}_{2\times 2} = DD^{\mathsf T}, \\ D &= \begin{bmatrix} 1 & 0\\ \rho & \sqrt{1-\rho^2} \end{bmatrix}_{2\times 2}, \\ g(t) &= D^{\mathsf T} \sigma^*_x H(t)^{-1}. \end{align*} The HJM forward rate vol is \begin{align*} \sigma(t, T) = g(t)h(T) = D^{\mathsf T}\begin{bmatrix} \sigma_1 e^{-\kappa_1 (T-t)} \\ \sigma_2 e^{-\kappa_2 (T-t)} \end{bmatrix}_{2\times 1}, \end{align*} or, if allowing a correlation \(\rho\) between the two driving Brownian motions of the forward rate process, just \begin{align*} \sigma^*(t, T) = \begin{bmatrix} \sigma_1 e^{-\kappa_1 (T-t)} \\ \sigma_2 e^{-\kappa_2 (T-t)} \end{bmatrix}_{2\times 1}. \end{align*}

Let \begin{align*} \sigma_x &= g(t)H(t) = \begin{bmatrix} \sigma_1 & \sigma_2\rho\\ 0 & \sigma_2 \sqrt{1-\rho^2} \end{bmatrix}_{2\times 2}.\\ \kappa &= \begin{bmatrix} \kappa_1 & 0\\ 0 & \kappa_2 \end{bmatrix}_{2\times 2}. \end{align*}

Then the short rate process is \(r(t) = f(0, t) + x_1(t) + x_2(t) = f(0, t) + x(t)\mathbf 1\), where \(x(0) = y(0) = 0\), \begin{align*} \begin{cases} dx(t) = (y(t)\mathbf 1 - \kappa x(t))dt + \sigma_x^{\mathsf T} dW(t)\\ dy(t) = (\sigma_x^{\mathsf T}\sigma_x - \kappa y(t) - y(t)\kappa) dt \\ dW_1(t)dW_2(t) = 0 \end{cases}, \end{align*} and the covariance matrix is \begin{align*} \sigma_x^{\mathsf T}\sigma_x = \begin{bmatrix} \sigma_1^2 & \rho\sigma_1\sigma_2 \\ \rho\sigma_1\sigma_2 & \sigma_2^2 \end{bmatrix}_{2\times 2}. \end{align*} The ODE of \(y(t)\) can be solved explicitly to obtain \begin{align*} y(t) &= H(t)\left(\int_0^t g(s)^{\mathsf T}g(s)\,ds\right)H(t)\\ &= \begin{bmatrix} \frac{\sigma_1^2\left(1-e^{-2\kappa_1 t}\right)}{2\kappa_1} & \frac{\rho\sigma_1\sigma_2\left(1-e^{-(\kappa_1 + \kappa_2) t}\right)}{\kappa_1 + \kappa_2}\\ \frac{\rho\sigma_1\sigma_2\left(1-e^{-(\kappa_1 + \kappa_2) t}\right)}{\kappa_1 + \kappa_2} & \frac{\sigma_2^2\left(1-e^{-2\kappa_2 t}\right)}{2\kappa_2} \end{bmatrix}_{2\times 2}. \end{align*} Alternatively, one can write \begin{align*} \begin{cases} dx(t) = (y(t)\mathbf 1 - \kappa x(t))dt + \sigma^*_x dW^*(t) \\ dW_1^*(t)dW_2^*(t) = \rho dt \end{cases}, \end{align*} or more explicitly, \begin{align*} \begin{cases} dx_1(t) = \left(\frac{\sigma_1^2\left(1-e^{-2\kappa_1 t}\right)}{2\kappa_1} + \frac{\rho\sigma_1\sigma_2\left(1-e^{-(\kappa_1 + \kappa_2) t}\right)}{\kappa_1 + \kappa_2} - \kappa_1 x_1(t)\right)dt + \sigma_1 dW^*_1(t) \\ dx_2(t) = \left(\frac{\sigma_2^2\left(1-e^{-2\kappa_2 t}\right)}{2\kappa_2} + \frac{\rho\sigma_1\sigma_2\left(1-e^{-(\kappa_1 + \kappa_2) t}\right)}{\kappa_1 + \kappa_2} - \kappa_2 x_2(t)\right)dt + \sigma_2 dW^*_2(t) \\ dW_1^*(t)dW_2^*(t) = \rho dt \end{cases}. \end{align*}

Let \begin{align*} M(t, T) &= H(T)H(t)^{-1}\mathbf 1 = \begin{bmatrix} e^{-\kappa_1(T-t)}\\ e^{-\kappa_2(T-t)} \end{bmatrix}_{2\times 1}, \\ G(t, T) &= \int_t^TM(t, u)\,du = \begin{bmatrix} \frac{1-e^{-\kappa_1(T-t)}}{\kappa_1}\\ \frac{1-e^{-\kappa_2(T-t)}}{\kappa_2} \end{bmatrix}_{2\times 1}. \end{align*} Then the forward rate process and the zero-coupon bond price are \begin{align*} f(t, T) &= f(0, T) + M(t, T)^{\mathsf T}(x(t) + y(t)G(t, T)), \\ P(t, T) &=\frac{P(0, T)}{P(0, t)}\exp\left(-G(t, T)^{\mathsf T}x(t) - \frac12G(t, T)^{\mathsf T}y(t)G(t, T)\right), \end{align*} respectively. Note that since \(G\) and \(M\) are both functions of \(T-t\), the dynamics of \(f(t, T)\) and \(P(t, T)\) are stationary.

The risk-neutral process of \(P(t, T)\) is log-normal \begin{align*} \frac{dP(t, T)}{P(t, T)} &= r(t)dt - (\sigma_x G(t, T))^{\mathsf T} dW(t)\\ &= r(t)dt - (\sigma^*_x G(t, T))^{\mathsf T} dW^*(t). \end{align*} That is, the HJM bond price vol is \(\Sigma(t, T) = \sigma_x G(t, T)\), or \begin{align*} \Sigma^*(t, T) = \sigma^*_x G(t, T) = \begin{bmatrix} \frac{\sigma_1}{\kappa_1}\left(1-e^{-\kappa_1(T-t)}\right)\\ \frac{\sigma_2}{\kappa_2}\left(1-e^{-\kappa_2(T-t)}\right) \end{bmatrix}_{2\times 1} \end{align*} if allowing a correlation \(\rho\) between the two Brownian motions in the process. The following identities hold: \begin{align*} \sigma_x^* M &= \sigma^*(t, T), \\ \sigma_x^* G &= \Sigma^*(t, T). \end{align*}

We note that the \(g(t)\) being a constant matrix times \(H(t)^{-1}\) makes the forward rate vol time stationary. In a HW1F with time stationary forward rate vol this is necessary, because if \begin{align*} \sigma(t, T) = g(t)h(T) = f(T-t) \end{align*} for some function \(f\), then we can write \begin{align*} \sigma(t, t) = g(t)h(t) = f(0) \end{align*} which is a constant. This constant is in fact the short rate vol which we denote by \(\sigma_r\), and we must have \(g(t) = \sigma_r h(t)^{-1}\).

Covariance of a Stochastic Vector Process

Consider an \(m\)-factor model with \(N\) state variables in a vector \(\vec X_t\) which satisfies \begin{align*} d\vec X_t = O(dt) + \sigma^{\mathsf T}\,d\vec W_t, \end{align*} where \(\sigma\) is an \(m\times N\) matrix and \(\vec W_t\) is the standard (independent) Brownian motion. Then the \(N\times N\) instantaneous covariance matrix of \(X_t\) is \begin{align*} \text{cov}(d\vec X_t) = \left(\sigma^{\mathsf T}\sigma\right)\,dt. \end{align*} In general, if \begin{align*} d\vec X_t = O(dt) + \sigma^{\mathsf T}\,d\vec Z_t \end{align*} and \(\text{cov}(d\vec Z_t) = R\,dt\) then \begin{align*} \text{cov}(d\vec X_t) = \left(\sigma^{\mathsf T}R\sigma\right)\,dt. \end{align*} In particular, if \(\vec Z_t = \vec W^*_t\) is a correlated Brownian motion with instantaneous correlation matrix \(R\), then the instantaneous covariance matrix of \(X_t\) is given by the same formula.

Now consider the special case \(N=1\), where \(X_t\) is simply a scalar stochastic process and \(\sigma\) is an \(m\)-dimensional vector. If \begin{align*} dX_t = O(dt) + \sigma^{\mathsf T}\,d\vec W_t, \end{align*} where \(\vec W_t\) is the standard (independent) Brownian motion in \(m\)-dimensions, then \begin{align*} \text{Var}(dX_t) = \left(\sigma^{\mathsf T}\sigma\right)\,dt. \end{align*} If instead \begin{align*} dX_t = O(dt) + \sigma^{\mathsf T}\,d\vec Z_t, \end{align*} where \(\vec Z_t\) has instantaneous covariance matrix \(R\) (for example a correlated Brownian motion), then \begin{align*} \text{Var}(dX_t) = \left(\sigma^{\mathsf T}R\sigma\right)\,dt. \end{align*}

An application is to compute the variance of the instantaneous forward curve in the HJM framework for a specific \(T\): \begin{align*} df(t, T) &= \sigma(t, T)^{\mathsf T}(\Sigma(t, T)\,dt + d{\widetilde W}(t)), \\ \text{Var}(df(t, T)) &= \sigma(t, T)^{\mathsf T}\sigma(t, T)\,dt. \end{align*}

Covariance of Instantaneous Forward Curve in Multi-Dimensional HJM

Consider an \(m\)-factor HJM model \begin{align*} df(t, T) &= \sigma(t, T)^{\mathsf T}(\Sigma(t, T)\,dt + d\widetilde W(t)) \\ &= {\sigma^*(t, T)}^{\mathsf T}(\Sigma^*(t, T)\,dt + d{\widetilde W}^*(t)), \end{align*} where \begin{align*} &\text{$\sigma(t, T)$ is an $m$-dimensional volatility vector, }\\ &\text{$\widetilde W(t)$ is the $m$-dimensional standard (independent) Brownian motion, } \end{align*} while \begin{align*} &\text{$\sigma^*(t, T)$ is an $N$-dimensional volatility vector, }\\ &\text{$\widetilde W^*(t)$ is $N$-dimensional with correlation matrix $R$. } \end{align*} If we write \(R = DD^{\mathsf T}\) with \(D\) an \(N\times m\) matrix then the following identity holds \begin{align*} \sigma(t, T) = D^{\mathsf T} \sigma^*(t, T). \end{align*} Modeling the volatility vector \(\sigma^*(t, T)\) and the correlation \(R\) separately is a simpler way than modeling the matrix \(\sigma(t, T)\) directly.

Let \begin{align*} \sigma^*(t, T) = \begin{pmatrix} \sigma_1^*(t, T)\\ \sigma_2^*(t, T)\\ \vdots\\ \sigma_N^*(t, T)\\ \end{pmatrix}. \end{align*} Most likely (?) it can be shown that if all \(\sigma_j^*(t, T)\) are separable then the short rate process is Markovian. Let \(S = \operatorname{diag}(\sigma^*(t, T))\). The factor covariance matrix is \(SRS\).

To compute the forward rates covariance matrix, consider the forward rates in \(M\) tenors \(\delta_1, \delta_2, \ldots, \delta_M\): \begin{align*} df(t, t+\delta_1) &= {\sigma^*(t, t+\delta_1)}^{\mathsf T}(\Sigma(t, t+\delta_1)\,dt + d{\widetilde W}^*(t)), \\ df(t, t+\delta_2) &= {\sigma^*(t, t+\delta_2)}^{\mathsf T}(\Sigma(t, t+\delta_2)\,dt + d{\widetilde W}^*(t)), \\ &\qquad\qquad\qquad\vdots\\ df(t, t+\delta_M) &= {\sigma^*(t, t+\delta_M)}^{\mathsf T}(\Sigma(t, t+\delta_M)\,dt + d{\widetilde W}^*(t)). \end{align*} Denote \(f_j(t) = f(t, t+\delta_j), ~\vec f(t) = (f_1(t), f_2(t), \ldots, f_M(t))^{\mathsf T}\). Then we can write the above in matrix form as \begin{align*} d\vec f(t) &= O(dt) + \begin{pmatrix} \frac{\quad}{\quad} & {\sigma^*(t, t+\delta_1)}^{\mathsf T} & \frac{\quad}{\quad}\\ \frac{\quad}{\quad} & {\sigma^*(t, t+\delta_2)}^{\mathsf T} & \frac{\quad}{\quad}\\ &\vdots&\\ \frac{\quad}{\quad} & {\sigma^*(t, t+\delta_M)}^{\mathsf T} & \frac{\quad}{\quad}\\ \end{pmatrix}_{M\times N}\,d{\widetilde W}^*(t)\\ &= O(dt) + \begin{pmatrix} \sigma_1^*(t, t+\delta_1) & \sigma_2^*(t, t+\delta_1) & \cdots & \sigma_N^*(t, t+\delta_1)\\ \sigma_1^*(t, t+\delta_2) & \sigma_2^*(t, t+\delta_2) & \cdots & \sigma_N^*(t, t+\delta_2)\\ \vdots & \vdots & \ddots & \vdots \\ \sigma_1^*(t, t+\delta_M) & \sigma_2^*(t, t+\delta_M) & \cdots & \sigma_N^*(t, t+\delta_M) \end{pmatrix}_{M\times N}\,d{\widetilde W}^*(t). \end{align*} We further denote the \(M\times N\) volatility matrix by \((\sigma_f^*)^{\mathsf T}\). The forward rates covariance matrix is then given by \((\sigma_f^*)^{\mathsf T}R\sigma_f^*\). Preferably the entire matrix is time stationary (function of \(\delta_j\)). A sufficient condition to achieve that is for each element \(\sigma_i^*(t, T)\) to be time stationary. Given the property of HW1F that the only possible time stationary separable vol is \(\sigma_re^{-k(T-t)}\), we know each \(\sigma_i^*(t, T)\) must have the same form. This leads to HWmF.

Each element \(\sigma_i^*(t, T)\) being time stationary is simply a sufficient condition for the forward rate covariance to be time stationary, not necessary. Is it possible there exists a model with time stationary forward rate covariance but each element \(\sigma_i^*(t, T)\) is not time stationary?

Covariance of Instantaneous Forward Curve in HWmF

Consider a 3-factor model. Recall that \begin{align*} f(t, T) = f(0, T) + M(t, T)^{\mathsf T}\left(x(t) + y(t) G(t, T)\right), \end{align*} where \begin{align*} M(t, T) &= H(T)H(t)^{-1}\mathbf 1 = \begin{bmatrix} e^{-\kappa_1(T-t)}\\ e^{-\kappa_2(T-t)}\\ e^{-\kappa_3(T-t)} \end{bmatrix}_{3\times 1}, \\ G(t, T) &= \int_t^TM(t, u)\,du = \begin{bmatrix} \frac{1-e^{-\kappa_1(T-t)}}{\kappa_1}\\ \frac{1-e^{-\kappa_2(T-t)}}{\kappa_2}\\ \frac{1-e^{-\kappa_2(T-t)}}{\kappa_2} \end{bmatrix}_{3\times 1}. \end{align*} Plug in \(T=t+\delta\) to write \begin{align*} f(t, t+\delta) &= f(0, t+\delta) + M(t, t+\delta)^{\mathsf T}\left(x(t) + y(t) G(t, t+\delta)\right), \\ &= f(0, t+\delta) + \begin{bmatrix}e^{-\kappa_1\delta} & e^{-\kappa_2\delta} & e^{-\kappa_3\delta}\end{bmatrix}\left(x(t) + y(t) G(t, t+\delta)\right). \end{align*} This is true for all \(\delta\), so we can write \begin{align*} f(t, t+\delta_1) &= f(0, t+\delta_1) + \begin{bmatrix}e^{-\kappa_1\delta_1} & e^{-\kappa_2\delta_1} & e^{-\kappa_3\delta_1}\end{bmatrix}\left(x(t) + y(t) G(t, t+\delta_1)\right), \\ f(t, t+\delta_2) &= f(0, t+\delta_2) + \begin{bmatrix}e^{-\kappa_1\delta_2} & e^{-\kappa_2\delta_2} & e^{-\kappa_3\delta_2}\end{bmatrix}\left(x(t) + y(t) G(t, t+\delta_2)\right), \\ &\vdots\\ f(t, t+\delta_M) &= f(0, t+\delta_M) + \begin{bmatrix}e^{-\kappa_1\delta_M} & e^{-\kappa_2\delta_M} & e^{-\kappa_3\delta_M}\end{bmatrix}\left(x(t) + y(t) G(t, t+\delta_M)\right). \end{align*} Denote \(f_j(t) = f(t, t+\delta_j), ~\vec f(t) = (f_1(t), f_2(t), \ldots, f_M(t))^{\mathsf T}\) and write the above in vector differential form, we obtain \begin{align*} d\vec f(t) = H_f^{\mathsf T} dx(t) + O(dt), \end{align*} where \begin{align*} H_f^{\mathsf T} = \begin{bmatrix} e^{-\kappa_1\delta_1} & e^{-\kappa_2\delta_1} & e^{-\kappa_3\delta_1}\\ e^{-\kappa_1\delta_2} & e^{-\kappa_2\delta_2} & e^{-\kappa_3\delta_2}\\ &\vdots&\\ e^{-\kappa_1\delta_M} & e^{-\kappa_2\delta_M} & e^{-\kappa_3\delta_M}\\ \end{bmatrix}_{M\times 3}. \end{align*} The \(H_f^{\mathsf T}\) matrix is denoted by \(H^f(0) = H^f(t)H(t)^{-1}\) in Leif Andersen p.577. Given the lemmas in the previous section, it is easy to compute the \(M\times M\) instantaneous covariance matrix of the forward curve \(\vec f(t)\) to be \begin{align*} H_f^{\mathsf T} R H_f, \end{align*} where \(R\) is the \(3\times 3\) factor covariance matrix in HW3F, denoted by \(\sigma_x^{\mathsf T}\sigma_x\) above.

Forward Rate and Instantaneous Forward Rate Covariance

Instantaneous forward rate has covariance

while the forward rate (with a tenor) has covariance

where the quantity in the product of two brackets is approximately

as each bracket is

HW2F PCA

Let \(X\) be a matrix with forward rate daily changes on each row. Then the forward curve sample covariance matrix is \begin{align*} \frac{1}{n}X^{\mathsf T}X. \end{align*} A singular value decomposition of \(X\) gives \begin{align*} X = USV^{\mathsf T} = TV^{\mathsf T}, \end{align*} where the column vectors of \(V\) are the principal components (PCs) and \(T\) is a matrix of PC scores. Thus the covariance matrix is \begin{align*} \frac{1}{n}X^{\mathsf T}X = VSU^{\mathsf T} USV^{\mathsf T} = V\left(\frac{S^2}{n}\right)V^{\mathsf T}. \end{align*} That is, a decomposition of the covariance matrix gives us the PCs.

We have shown the forward rate covariance matrix in HW2F to be \begin{align*} H_f^{\mathsf T} R H_f, \end{align*} where \begin{align*} H_f = \begin{bmatrix} e^{-\kappa_1\delta_1} & e^{-\kappa_1\delta_2} & \cdots & e^{-\kappa_1\delta_M}\\ e^{-\kappa_2\delta_1} & e^{-\kappa_2\delta_2} & \cdots & e^{-\kappa_2\delta_M} \end{bmatrix}_{M\times 2}. \end{align*} From now on we denote by \(h_1^{\mathsf T}\) and \(h_2^{\mathsf T}\) the \(M\)-dimensional row vectors of \(H_f\) and write \begin{align*} H_f = \begin{bmatrix} \frac{\qquad}{\qquad} & h_1 & \frac{\qquad}{\qquad}\\ \frac{\qquad}{\qquad} & h_2 & \frac{\qquad}{\qquad}\\ \end{bmatrix}_{M\times 2}. \end{align*} We can rewrite the covariance matrix as \begin{align*} &H_f^{\mathsf T} \begin{bmatrix} \sigma_1 & 0\\ 0 & \sigma_2 \end{bmatrix} \begin{bmatrix} 1 & \rho\\ \rho & 1 \end{bmatrix} \begin{bmatrix} \sigma_1 & 0\\ 0 & \sigma_2 \end{bmatrix} H_f \\ =& H_f^{\mathsf T} \begin{bmatrix} \sigma_1 & 0\\ 0 & \sigma_2 \end{bmatrix} \begin{bmatrix} \frac{1}{\sqrt{2}} & \frac{1}{\sqrt{2}}\\ -\frac{1}{\sqrt{2}} & \frac{1}{\sqrt{2}}\\ \end{bmatrix} \begin{bmatrix} 1-\rho & 0\\ 0 & 1+\rho \end{bmatrix} \begin{bmatrix} \frac{1}{\sqrt{2}} & -\frac{1}{\sqrt{2}}\\ \frac{1}{\sqrt{2}} & \frac{1}{\sqrt{2}}\\ \end{bmatrix} \begin{bmatrix} \sigma_1 & 0\\ 0 & \sigma_2 \end{bmatrix} H_f. \end{align*} Thus \begin{align*} \frac{S}{\sqrt n}V^{\mathsf T} &= \begin{bmatrix} \sqrt{\frac{1-\rho}{2}} & 0\\ 0 & \sqrt{\frac{1+\rho}{2}} \end{bmatrix} \begin{bmatrix} 1 & -1\\ 1 & 1 \end{bmatrix} \begin{bmatrix} \sigma_1 & 0\\ 0 & \sigma_2 \end{bmatrix} \begin{bmatrix} \frac{\qquad}{\qquad} & h_1 & \frac{\qquad}{\qquad}\\ \frac{\qquad}{\qquad} & h_2 & \frac{\qquad}{\qquad}\\ \end{bmatrix}_{M\times 2}\\ &= \begin{bmatrix} \sqrt{\frac{1-\rho}{2}} & 0\\ 0 & \sqrt{\frac{1+\rho}{2}} \end{bmatrix} \begin{bmatrix} \frac{\qquad}{\qquad} & \sigma_1 h_1 - \sigma_2 h_2 & \frac{\qquad}{\qquad}\\ \frac{\qquad}{\qquad} & \sigma_1 h_1 + \sigma_2 h_2 & \frac{\qquad}{\qquad}\\ \end{bmatrix}_{M\times 2}, \end{align*} so PC1 and PC2 are \begin{align*} \frac{\sigma_1 h_1 - \sigma_2 h_2}{\lVert \sigma_1 h_1 - \sigma_2 h_2\rVert}, \qquad \frac{\sigma_1 h_1 + \sigma_2 h_2}{\lVert \sigma_1 h_1 + \sigma_2 h_2\rVert}, \end{align*} respectively, while their corresponding score standard deviations are \begin{align*} \sqrt{\frac{1-\rho}{2}}\lVert \sigma_1 h_1 - \sigma_2 h_2\rVert, \qquad\sqrt{\frac{1+\rho}{2}} \lVert \sigma_1 h_1 + \sigma_2 h_2\rVert, \end{align*} respectively. A well known property of HW2F is that \(\rho\) needs to be close to -1 to capture volatility hump. Consistently, here \(\rho\) also needs to be close to -1 for PC1 score standard deviations to be much larger than PC2’s.

Writing as a continuous function of \(\tau\), PC1 is scaled \begin{align*} \sigma_1e^{-\kappa_1\tau} - \sigma_2e^{-\kappa_2\tau} \end{align*} and PC2 is scaled \begin{align*} \sigma_1e^{-\kappa_1\tau} + \sigma_2e^{-\kappa_2\tau}. \end{align*} For PC1 to be close to a flat function, we must have \(\kappa_1 \approx \kappa_2\), \(\sigma_1 \approx \sigma_2\), or \(\kappa_1\) and \(\kappa_2\) both tiny.

HW1F Summary

Let \(h(t) = e^{-\kappa t}, g(t) = \sigma e^{\kappa t}\). The HJM forward rate vol is \begin{align*} \sigma(t, T) = g(t)h(T) = \sigma e^{-\kappa (T-t)}. \end{align*}

The short rate process is \(r(t) = f(0, t) + x(t)\), where \(x(0) = y(0) = 0\), \begin{align*} \begin{cases} dx(t) = (y(t) - \kappa x(t))dt + \sigma dW(t)\\ dy(t) = (\sigma^2 - 2\kappa y(t)) dt \end{cases}. \end{align*} The ODE of \(y(t)\) can be solved explicitly to obtain \begin{align*} y(t) &= h^2(t)\int_0^t g^2(s)\,ds = \frac{\sigma^2\left(1-e^{-2\kappa t}\right)}{2\kappa}. \end{align*} Let \begin{align*} M(t, T) &= h(T)h(t)^{-1} = e^{-\kappa(T-t)}, \\ G(t, T) &= \int_t^TM(t, u)\,du = \frac{1-e^{-\kappa(T-t)}}{\kappa}. \end{align*} Note that \begin{align*} \sigma M(t, T) &= \sigma(t, T) = \sigma e^{-\kappa(T-t)}, \\ \sigma G(t, T) &= \Sigma(t, T) = \frac{\sigma\left(1-e^{-\kappa(T-t)}\right)}{\kappa} \end{align*} are HJM forward rate vol and bond price vol, respectively. The forward rate process and the zero-coupon bond price in HW1F are \begin{align*} f(t, T) &= f(0, T) + M(t, T)(x(t) + y(t)G(t, T)), \\ P(t, T) &=\frac{P(0, T)}{P(0, t)}\exp\left(-G(t, T)x(t) - \frac12G^2(t, T)y(t)\right), \end{align*} respectively. Note that since \(G\) and \(M\) are both functions of \(T-t\), the dynamics of \(f(t, T)\) and \(P(t, T)\) are stationary. More explicitly, one can write \(r(t) = f(0, t) + x(t)\), \(x(0) = 0\), \begin{align*} dx(t) &= \left(\frac{\sigma^2\left(1-e^{-2\kappa t}\right)}{2\kappa} - \kappa x(t)\right)dt + \sigma dW(t), \\ f(t, T) &= f(0, T) + e^{-\kappa(T-t)}\left(x(t) + \frac{\sigma^2\left(1-e^{-2\kappa t}\right)\left(1-e^{-\kappa(T-t)}\right)}{2\kappa^2}\right), \\ P(t, T) &=\frac{P(0, T)}{P(0, t)}\exp\left(-\frac{1-e^{-\kappa(T-t)}}{\kappa}x(t) - \frac{\sigma^2\left(1-e^{-2\kappa t}\right)\left(1-e^{-\kappa(T-t)}\right)^2}{4\kappa^3}\right). \end{align*}

The risk-neutral process of \(P(t, T)\) is log-normal \begin{align*} \frac{dP(t, T)}{P(t, T)} &= r(t)dt - \sigma G(t, T) dW(t). \end{align*}

Mid-Curve Swaption Pricing

Consider a 1y5y5y midcurve, which is an option on a 5y5y forward swap, that expires 1y from today. The 5y5y forward swap’s terms only start counting 1y from today, so the end date of the trade is 11y from today. Please draw the timeline on paper yourself to better understand the below argument. Since the underlying swap is really 6y5y, the NPV is

But the important thing to note is that \(T=1Y\), and that vol for \(S_{6\times 5}(T=1Y)\) is not quoted. Only vol for \(S_{6\times 5}(T=6Y)\) is quoted. Thus we rewrite the payoff \(A_{6\times 5}(T)(S_{6\times 5}(T) - K)^+\) in terms of 1y5y and 1y10y swap rates, both with vol quoted in the market. Note that \begin{align*} S_{6\times 5}(t) &= \frac{P(t, T=6Y) - P(t, T=11Y)}{A_{6\times 5}(t)}, \\ S_{1\times 5}(t) &= \frac{P(t, T=1Y) - P(t, T=6Y)}{A_{1\times 5}(t)}, \\ S_{1\times 10}(t) &= \frac{P(t, T=1Y) - P(t, T=11Y)}{A_{1\times 10}(t)}. \end{align*} Thus we can write

or equivalently,

and the NPV of the mid-curve is \begin{align*} &M(0) \widetilde E\left[ \frac{1}{M(T)} A_{6\times 5}(T) (S_{6\times 5}(T) - K)^+\right]\\ =& M(0) \widetilde E\left[ \frac{1}{M(T)} A_{6\times 5}(T) \left(\frac{A_{1\times 10}(T)}{A_{6\times 5}(T)}S_{1\times 10}(T) - \frac{A_{1\times 5}(T)}{A_{6\times 5}(T)}S_{1\times 5}(T) - K\right)^+\right] \\ =& A_{6\times 5}(0) E^{A_{6\times 5}}\left[\left(\frac{A_{1\times 10}(T)}{A_{6\times 5}(T)}S_{1\times 10}(T) - \frac{A_{1\times 5}(T)}{A_{6\times 5}(T)}S_{1\times 5}(T) - K\right)^+\right] \\ \approx& A_{6\times 5}(0) E^{A_{6\times 5}}\left[\left(\frac{A_{1\times 10}(0)}{A_{6\times 5}(0)}S_{1\times 10}(T) - \frac{A_{1\times 5}(0)}{A_{6\times 5}(0)}S_{1\times 5}(T) - K\right)^+\right]. \end{align*} The last approximation says, I don’t know the annuity ratio one year from now so I’m just going to use today’s. This might not be accurate but that’s what every one does anyways. The annuity ratio itself is a martingale:

but that does not justify the freezing.

Forward Swap Rate Correlation for Mid-Curve

If we have forward rate correlation \(\text{corr}(L_n(T), L_m(T))\) estimated, this is how to translate it to forward swap rate correlation: \begin{align*} \text{corr}(S_{1\times 5}(T), S_{1\times 10}(T)) &= \frac{1}{\sigma_{1\times 5}(T)\sqrt{T}\cdot\sigma_{1\times 10}(T)\sqrt{T}} \text{cov}(S_{1\times 5}(T), S_{1\times 10}(T))\\ &= \frac{1}{\sigma_{1\times 5}(T)\sqrt{T}\cdot\sigma_{1\times 10}(T)\sqrt{T}} \text{cov}\left(\frac{\sum_{1\times 5}\tau_n P(T, T_{n+1})L_n(T)}{A_{1\times 5}(T)}, \frac{\sum_{1\times 10}\tau_m P(T, T_{m+1})L_m(T)}{A_{1\times 10}(T)}\right)\\ &\approx \frac{1}{\sigma_{1\times 5}(T)\sqrt{T}\cdot\sigma_{1\times 10}(T)\sqrt{T}\cdot A_{1\times 5}(0)A_{1\times 10}(0)} \sum_{1\times 5} \sum_{1\times 10} \tau_n \tau_m P(0, T_{n+1}) P(0, T_{m+1})\text{cov}(L_n(T), L_m(T))\\ &= \frac{1}{\sigma_{1\times 5}(T)\sqrt{T}\cdot\sigma_{1\times 10}(T)\sqrt{T}\cdot A_{1\times 5}(0)A_{1\times 10}(0)} \sum_{1\times 5} \sum_{1\times 10} \tau_n \tau_m P(0, T_{n+1}) P(0, T_{m+1})\sigma_n(T)\sqrt{T}\cdot\sigma_m(T)\sqrt{T}\cdot\text{corr}(L_n(T), L_m(T))\\ &= \frac{1}{\sigma_{1\times 5}(T)\sigma_{1\times 10}(T) A_{1\times 5}(0)A_{1\times 10}(0)} \sum_{1\times 5} \sum_{1\times 10} \tau_n \tau_m P(0, T_{n+1}) P(0, T_{m+1})\sigma_n(T)\sigma_m(T)\text{corr}(L_n(T), L_m(T)). \end{align*} Here we need \(T=1Y\). The \(\sigma_{1\times 5}(T)\) and \(\sigma_{1\times 10}(T)\) in the denominator are from the swaption vol surface. The \(\sigma_n(T)\) and \(\sigma_m(T)\) in the summation are vols of the one year tenor forward rate (\(L(t, T_m, T_{m+1})\) with \(T_{m+1} = T_m + 1\)), which is equivalent to the first column of the swaption vol surface \(\sigma_{n\times 1}(T), \sigma_{m\times 1}(T)\), but we will have the same issue as in mid-curve pricing: \(\sigma_{n\times 1}(T=1Y)\) is not quoted, only \(\sigma_{n\times 1}(T=n \text{ years})\) is.

Replication Formula

Note that \begin{align*} f(S) &= f(K_0) + \int_{K_0}^S f'(K)\,dK\\ &= f(K_0) -\int_{\mathbb R} 1_{\{S\le K\le K_0\}} f'(K)\,dK + \int_{\mathbb R} 1_{\{K_0\le K\le S\}} f'(K)\,dK, \end{align*} where the last two terms cannot to be both nonzero. The first term is nonzero only if \(K_0> S\) and the second term is nonzero only if \(K_0< S\). We can rewrite \begin{align*} f(S) =& ~f(K_0) -\int_0^{K_0} 1_{\{K\ge S\}} f'(K)\,dK + \int_{K_0}^\infty 1_{\{K\le S\}} f'(K)\,dK\\ =& ~f(K_0) + \int_0^{K_0} (K-S)^+ f''(K)\,dK + \int_{K_0}^\infty (S-K)^+ f''(K)\,dK\\ &-\left[(K-S)^+ f'(K)\right]_{K=0}^{K=K_0} -\left[(S-K)^+ f'(K)\right]_{K=K_0}^{K=\infty}\\ %=& ~f(K_0) + \int_0^{K_0} (K-S)^+ f''(K)\,dK + \int_{K_0}^\infty (S-K)^+ f''(K)\,dK\\ %& - (K_0 - S)^+f'(K_0) + (S-K_0)^+ f'(K_0)\\ =& ~f(K_0) + (S-K_0) f'(K_0) + \int_0^{K_0} (K-S)^+ f''(K)\,dK + \int_{K_0}^\infty (S-K)^+ f''(K)\,dK. \end{align*} Now plug in \(S=S_T\) a random varaible and take expectation to obtain \begin{align*} E[f(S_T)] = f(K_0) + f'(K_0) E[S_T-K_0] + \int_0^{K_0} E[(K-S_T)^+] f''(K)\,dK + \int_{K_0}^\infty E[(S_T-K)^+] f''(K)\,dK. \end{align*} If we choose to set \(K_0 = E[S_T]\) (ATMF), the second term on the right hand side vanishes and we have \begin{align*} E[f(S_T)] = f(E[S_T]) + \int_0^{K_0} E[(K-S_T)^+] f''(K)\,dK + \int_{K_0}^\infty E[(S_T-K)^+] f''(K)\,dK. \end{align*}

Time Integral of Brownian Motion and Brownian Bridge

The integral form of \(d(tW_t) = W_tdt + tdW_t\) leads to \begin{align*} \int_0^T W_t\,dt = TW_T - \int_0^T t\,dW_t = \int_0^T T-t\,dW_t, \end{align*} so the integral of a Brownian bridge is \begin{align*} \int_0^T W_t - \frac{t}{T}W_T\,dt &=\int_0^T T-t\,dW_t - \left(\int_0^T\frac{t}{T}\,dt\right)W_T\\ &= \int_0^T T-t\,dW_t - \frac{T}{2} W_T\\ &= \int_0^T T-t-\frac{T}{2}\,dW_t \\ &= \int_0^T \frac{T}{2} - t\,dW_t \\ &\sim N\left(0, \int_0^T \left(\frac{T}{2} - t\right)^2\,dt\right) = N\left(0, \frac{T^3}{12}\right). \end{align*}

Time Integral of a Stochastic Process Given Two End Points

Let \(X(t)\) be the solution to the SDE \begin{align*} dX(t) &= \mu(t, X(t))\,dt + \sigma(t, X(t))\,dW(t). \end{align*} The goal is to find an approximating distribution of its time integral \begin{align*} \int_{t_1}^{t_2}X(t)\,dt \end{align*} under the condition \(X(t_1) = a\), \(X(t_2) = b\).

First we define \begin{align*} Y(t) = (X(t) - X(t_1)) - \frac{t - t_1}{t_2 - t_1}(X(t_2) - X(t_1)), \end{align*} which satisfies \(Y(t_1) = Y(t_2) = 0\). Next define \begin{align*} Y^{a\rightarrow b}(t) &= a + \frac{(b-a)(t-t_1)}{t_2 - t_1} + Y(t), \end{align*} which satisfies our conditions at both end points: \(Y^{a\rightarrow b}(t_1) = a, Y^{a\rightarrow b}(t_2) = b\). So the goal now is to find an approximating distribution of the integral \begin{align*} \int_{t_1}^{t_2} Y^{a\rightarrow b}(t)\, dt &= \int_{t_1}^{t_2} a + \frac{(b-a)(t-t_1)}{t_2 - t_1} + Y(t)\,dt\\ % &= \int_{t_1}^{t_2} a + \frac{(b-a)(t-t_1)}{t_2 - t_1} \,dt + \int_{t_1}^{t_2} (X(t) - X(t_1)) - \frac{t - t_1}{t_2 - t_1}(X(t_2) - X(t_1))\,dt\\ &= \frac{(a+b)(t_2 - t_1)}{2} + \int_{t_1}^{t_2} Y(t)\,dt. \end{align*} To find the integral of \(Y(t)\), we first need to compute the integral of \(X(t)\). Note that the integral form of \(d(tX(t)) = X(t)\,dt + t\,dX(t)\) leads to \begin{align*} \int_0^T X(t)\,dt = TX(T) - \int_0^T t\,dX(t) = \int_0^T T-t\,dX(t). \end{align*} This is true for all \(T>0\), so we can write \begin{align*} \int_0^{t_2} X(t)\,dt &= \int_0^{t_2} t_2-t\,dX(t), \\ \int_0^{t_1} X(t)\,dt &= \int_0^{t_1} t_1-t\,dX(t), \end{align*} and hence \begin{align*} \int_{t_1}^{t_2} X(t)\,dt &= \int_0^{t_2} t_2-t\,dX(t) - \int_0^{t_1} t_1-t\,dX(t). \end{align*} Thus the integral of \(Y(t)\) can be computed as follows: \begin{align*} \int_{t_1}^{t_2} Y(t)\,dt &= \int_{t_1}^{t_2} (X(t) - X(t_1)) - \frac{t - t_1}{t_2 - t_1}(X(t_2) - X(t_1))\,dt\\ &= \int_0^{t_2} t_2-t\,dX(t) - \int_0^{t_1} t_1-t\,dX(t) - X(t_1) \int_{t_1}^{t_2}\,dt - (X(t_2) - X(t_1)) \int_{t_1}^{t_2} \frac{t - t_1}{t_2 - t_1}\,dt\\ &= \int_0^{t_2} t_2-t\,dX(t) - \int_0^{t_1} t_1-t\,dX(t) - (t_2 - t_1)X(t_1) - \frac{t_2 - t_1}{2}(X(t_2) - X(t_1))\\ &= \int_0^{t_2} t_2-t\,dX(t) - \int_0^{t_1} t_1-t\,dX(t) - \frac{t_2 - t_1}{2}X(t_2) - \frac{t_2 - t_1}{2}X(t_1)\\ &= \int_0^{t_2} t_2 - \frac{t_2 - t_1}{2} -t\,dX(t) - \int_0^{t_1} t_1 + \frac{t_2 - t_1}{2} - t\,dX(t)\\ &= \int_0^{t_2} \frac{t_2 + t_1}{2} -t\,dX(t) - \int_0^{t_1} \frac{t_2 + t_1}{2} - t\,dX(t)\\ &= \int_{t_1}^{t_2} \frac{t_2 + t_1}{2} -t\,dX(t). \end{align*} We define \(t_{\text{mid}} = (t_2 + t_1)/2\) and write \begin{align*} \int_{t_1}^{t_2} Y(t)\,dt = \int_{t_1}^{t_2} (t_{\text{mid}} -t)\,dX(t). \end{align*} Note that, with \(Y(t)\) having the property \(Y(t_1) = Y(t_2) = 0\), the time integral of a Brownian bridge \begin{align*} \int_{0}^{T} W(t) - \frac{t}{T} W(T)\,dt = \int_{0}^{T} \left(\frac{T}{2} -t\right)\,dW(t) \end{align*} is simply a special case of the above result. Next we expand \(dX(t)\) to obtain \begin{align*} \int_{t_1}^{t_2} Y(t)\,dt = \int_{t_1}^{t_2} \left(t_{\text{mid}} -t\right) \mu(t, X(t))\,dt + \int_{t_1}^{t_2} \left(t_{\text{mid}} -t\right) \sigma(t, X(t))\,dW(t). \end{align*} Thus \begin{align*} \int_{t_1}^{t_2} Y^{a\rightarrow b}(t)\, dt &= \frac{(a+b)(t_2 - t_1)}{2} + \int_{t_1}^{t_2} \left(t_{\text{mid}} -t\right) \mu(t, X(t))\,dt + \int_{t_1}^{t_2} \left(t_{\text{mid}} -t\right) \sigma(t, X(t))\,dW(t). \end{align*} From here we would need some kind of approximation. The simplest one would be to replace processes \(\mu(t, X(t))\) and \(\sigma(t, X(t))\) in the integrand by their initial values and write \begin{align*} \int_{t_1}^{t_2} Y^{a\rightarrow b}(t)\, dt &\approx \frac{(a+b)(t_2 - t_1)}{2} + \int_{t_1}^{t_2} \left(t_{\text{mid}} -t\right) \mu(t_1, a)\,dt + \int_{t_1}^{t_2} \left(t_{\text{mid}} -t\right) \sigma(t_1, a)\,dW(t)\\ &= \frac{(a+b)(t_2 - t_1)}{2} + \sigma(t_1, a)\int_{t_1}^{t_2} \left(t_{\text{mid}} -t\right) \,dW(t)\\ &\sim N\left(\frac{(a+b)(t_2 - t_1)}{2}, \sigma^2(t_1, a)\int_{t_1}^{t_2} \left(t_{\text{mid}} -t\right)^2 \,dt\right) \\ &= N\left(\frac{(a+b)(t_2 - t_1)}{2}, \frac{\sigma^2(t_1, a)(t_2 - t_1)^3}{12}\right). \end{align*} The initial values of the processes \(\mu(t, X(t))\) and \(\sigma(t, X(t))\) are simply the first term of their corresponding Ito-Taylor expensions. More accurate (and non-Gaussian) approximations can be obtained by expanding them to a higer order, similar to the Milstein Scheme.

Another idea to find an approximating distribution is to replace the \(X(t)\) in \(\mu(t, X(t))\) and \(\sigma(t, X(t))\) by a deterministic function \(\bar X(t)\). One can use for example the solution to the ODE \begin{align*} d\bar X(t) &= \mu(t, \bar X(t))\,dt, \\ X(t_1) &= a, \end{align*} which is equal to \(E[X(t)]\) if \(\mu(t, X(t))\) is affine in \(X(t)\), since \begin{align*} E[X(t)] &= E\left[X(t_1) + \int_{t_1}^t \mu(s, X(s))\,ds + \int_{t_1}^t \sigma(s, X(s))\,dW(s)\right]\\ &= X(t_1) + \int_{t_1}^t \mu(s, E[X(s)])\,ds. \end{align*} When \(\mu(t, X(t))\) is not affine in \(X(t)\), the last equation does not hold and \(\bar X(t)\) is not equal to \(E[X(t)]\). It is only an approximation. For most \(\mu\) functions used in practice, the ODE of \(\bar X(t)\) can be solved analytically. When this is not the case, one can always introduce one extra layer of approximation and use the series expansion \begin{align*} \bar X(t) = a + \mu(t_1, a)(t - t_1). \end{align*} Once we determine an \(\bar X(t)\) function, we can write the approximation \begin{align*} \int_{t_1}^{t_2} Y^{a\rightarrow b}(t)\, dt &\approx \frac{(a+b)(t_2 - t_1)}{2} + \int_{t_1}^{t_2} \left(t_{\text{mid}} -t\right) \mu(t, \bar X(t))\,dt + \int_{t_1}^{t_2} \left(t_{\text{mid}} -t\right) \sigma(t, \bar X(t))\,dW(t) \\ &\sim N\left(\frac{(a+b)(t_2 - t_1)}{2} + \int_{t_1}^{t_2} \left(t_{\text{mid}} -t\right) \mu(t, \bar X(t))\,dt, \int_{t_1}^{t_2} \left(t_{\text{mid}} -t\right)^2 \sigma^2(t, \bar X(t))\,dt\right). \end{align*} Note that when \(\mu(t, X(t))\) is affine in \(X(t)\), the mean of the above distribution is the exact mean of \(\int_{t_1}^{t_2} Y^{a\rightarrow b}(t)\,dt\), not an approximation, as \begin{align*} E\left[\int_{t_1}^{t_2} Y^{a\rightarrow b}(t)\, dt\right] &= E\left[\frac{(a+b)(t_2 - t_1)}{2} + \int_{t_1}^{t_2} \left(t_{\text{mid}} -t\right) \mu(t, X(t))\,dt + \int_{t_1}^{t_2} \left(t_{\text{mid}} -t\right) \sigma(t, X(t))\,dW(t)\right] \\ &= \frac{(a+b)(t_2 - t_1)}{2} + \int_{t_1}^{t_2} \left(t_{\text{mid}} -t\right) E[\mu(t, X(t))]\,dt\\ &= \frac{(a+b)(t_2 - t_1)}{2} + \int_{t_1}^{t_2} \left(t_{\text{mid}} -t\right) \mu(t, E[X(t)])\,dt. \end{align*} When \(\mu(t, X(t))\) is not affine in \(X(t)\), if \(E[\mu(t, X(t))]\) is known, the exact mean can still be found.

Skip Bump and Recalibrate

Let \(f(x): \mathbb R^m \longmapsto \mathbb R^n\) be a pricing function with fixed market input, and \(x\in \mathbb R^m\) a vector of model parameters. Let \(b\in\mathbb R^n\) be the benchmart (target prices). We have found \(x^*\) such that \(f(x^*)\) is as close to the benchmark \(b\) as possible. Denote such \(x^*\) as \(x^*(b)\). With small perturbation \(\delta\) to the benchmark, the calibration result changes to \begin{align*} x^*(b+\delta) \approx x^*(b) + \left(J^{\mathsf T}J\right)^{-1}J^{\mathsf T}\delta, \end{align*} where \(J = Jf(x^*(b))\) is the \(n\times m\) Jacobian matrix of \(f\) at \(x^*(b)\). Note that \(n\ge m\) must hold for \(J^{\mathsf T}J\) to be invertible.

Convolution Pricing

To simplify the argument, let \(r=0\). Define \begin{align*} c(t, x) = E[Z|W_t = x] = E[Z|\mathcal F_t] \end{align*} to be the fair price of some derivative with payoff \(Z\). Thus for \(s < t\), we have \begin{align*} c(s, x) &= E[Z|W_s = x] = E[E[Z|\mathcal F_t]|\mathcal F_s]\\ &= E[c(t, W_t)|W_s = x]. \end{align*} Now write \(W_t = W_s + (W_t - W_s) = x + z\) and note that in \(\mathcal F_s\), \(z\) has a normal distribution \(N(0, t-s)\). Thus \begin{align*} c(s, x) &= \int_{-\infty}^{\infty} c(t, x+z) \frac{1}{\sqrt{2\pi(t-s)}} e^{-\frac{z^2}{2(t-s)}}\,dz\\ &= \int_{-\infty}^{\infty} c(t, y) \frac{1}{\sqrt{2\pi(t-s)}} e^{-\frac{(x-y)^2}{2(t-s)}}\,dz\\ &= c(t, x)\otimes p(x), \end{align*} where \(\otimes\) represents the convolution and \(p(x)\) is the probability density function of \(N(0, t-s)\).

SABR Normal Implied Volatility

\begin{align*} \begin{cases} dF_t = \alpha_tF_t^{\beta}\,dW_t\\ d\alpha_t = \nu \alpha_t\,dZ_t, \qquad \alpha_0 = \alpha\\ dW_tdZ_t = \rho dt \end{cases} \end{align*}

這裡用的是和 Hagan paper 一樣的符號,除了 \(W_t\) 和 \(Z_t\) 原 paper 是用 \(W_1\) 和 \(W_2\)

Code from pysabr,有和自己 implement 的 normal vol 對過結果一樣

\(F_0\) 用的是 \(t=0\) ATM forward rate

和書上一致:

\(\beta\) 和 \(\rho\) 控制 IV skew

\(\nu\) 控制 IV convexity

\(\alpha\) 控制 IV level

實測 \(\beta\) 除了會改變 skew 之外也會影響 IV level,而且影響幅度遠大於 \(\alpha\) 對 level 的影響

\(\beta\) 會影響 IV level 是因為 \(F_t \ll 1\),所以 \(\beta\) 越接近 \(0\),local volatility \(F_t^{\beta}\) 就越大,結果就是 option PV 和 IV 都變大

\(\rho\) 對 skew 的控制比 \(\beta\) 效果明顯多了,所以 LMM 固定 \(\rho=0\) 之後沒辦法 fit 任意 skew

若 \(\rho\gg 0\),同樣 moneyness 的 call 比 put 貴,因為等 \(F_t\) 漲到這個 call 變成 ATM 時 volatility \(\alpha_t\) 也變大了。結果就是 IV 右邊較高

若 \(\rho\ll 0\),同樣 moneyness 的 put 比 call 貴,因為等 \(F_t\) 跌到這個 put 變成 ATM 時 volatility \(\alpha_t\) 也變大了。結果就是 IV 左邊較高

[3]:

import numpy as np

def _f_minus_k_ratio(f, k, beta):

"""Hagan's 2002 f minus k ratio - formula (B.67a)."""

eps = 1e-07 # Numerical tolerance for f-k and beta

if abs(f-k) > eps:

if abs(1-beta) > eps:

return (1 - beta) * (f - k) / (f**(1-beta) - k**(1-beta))

else:

return (f - k) / np.log(f / k)

else:

return k**beta

def _zeta_over_x_of_zeta(k, f, t, alpha, beta, rho, volvol):

"""Hagan's 2002 zeta / x(zeta) function - formulas (B.67a)-(B.67b)."""

eps = 1e-07 # Numerical tolerance for zeta

f_av = np.sqrt(f * k)

zeta = volvol * (f - k) / (alpha * f_av**beta)

if abs(zeta) > eps:

return zeta / _x(rho, zeta)

else:

# The ratio converges to 1 when zeta approaches 0

return 1.

def _x(rho, z):

"""Hagan's 2002 x function - formula (B.67b)."""

a = (1 - 2*rho*z + z**2)**.5 + z - rho

b = 1 - rho

return np.log(a / b)

def normal_vol(k, f, t, alpha, beta, rho, volvol):

"""Hagan's 2002 SABR normal vol expansion - formula (B.67a)."""

# We break down the complex formula into simpler sub-components

f_av = np.sqrt(f * k)

A = - beta * (2 - beta) * alpha**2 / (24 * f_av**(2 - 2 * beta))

B = rho * alpha * volvol * beta / (4 * f_av**(1 - beta))

C = (2 - 3 * rho**2) * volvol**2 / 24

FMKR = _f_minus_k_ratio(f, k, beta)

ZXZ = _zeta_over_x_of_zeta(k, f, t, alpha, beta, rho, volvol)

# Aggregate all components into actual formula (B.67a)

v_n = alpha * FMKR * ZXZ * (1 + (A + B + C) * t)

return v_n

[4]:

import numpy as np

import matplotlib.pyplot as plt

from scipy.stats import norm

from pandas import DataFrame

from ipywidgets import interact

import warnings

warnings.filterwarnings('ignore')

@interact(F=(0.08, 0.15, 0.001), T=(1, 5, 1), alpha=(0.001, 0.01, 0.001), beta=(0.01, 0.99, 0.1), rho=(-0.99, 0.99, 0.1), volvol=(0.01, 1, 0.1))

def plot(F=0.1, T=1, alpha=0.01, beta=0.6, rho=0., volvol=0.6):

a = 0.08

b = 0.12

fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(16, 5))

def call(K, F, T, A=1):

iv = normal_vol(K, F, T, alpha, beta, rho, volvol)

d = (F-K)/(iv*np.sqrt(T))

return A*iv*np.sqrt(T)*(norm.pdf(d) + d*norm.cdf(d))

def put(K, F, T, A=1):

return call(K, F, T, A) + A*(K-F)

DataFrame([(K, normal_vol(K, F, T, alpha, beta, rho, volvol)) for K in np.arange(a, b, 0.01)], columns=['K', 'Implied Vol']).set_index('K').plot(style='-.', legend=None, ax=ax1)

ax1.set(ylim=(-0.001, 0.015), title='SABR Normal Implied Vol')

DataFrame([(K, call(K, F, T) if K>F else put(K, F, T)) for K in np.arange(a, b, 0.001)], columns=['K', 'OTM Options']).set_index('K').plot(style='-.', legend=None, ax=ax2)

ax2.set(ylim=(-0.0001, 0.0012), title='OTM Option PV')

plt.show()

Cython Version

初值會跑掉

感覺有快一點點

計算 PV 和 IV 都改用 Cython,用 c 的 pow,sqrt 和 log 取代 np 裡的,畫圖跳過 DataFrame 直接 ax.plot

如果 c function 能直接 output 二維 array 應該能再更快

[1]:

%load_ext cython

[2]:

%%cython

import numpy as np

import matplotlib.pyplot as plt

from scipy.stats import norm

from pandas import DataFrame

from ipywidgets import interact

from libc.math cimport pow, sqrt, log

import warnings

warnings.filterwarnings('ignore')

cdef double _cy_f_minus_k_ratio(double f, double k, double beta):

"""Hagan's 2002 f minus k ratio - formula (B.67a)."""

cdef double eps = 1e-07 # Numerical tolerance for f-k and beta

if abs(f-k) > eps:

if abs(1-beta) > eps:

return (1 - beta) * (f - k) / (pow(f, (1-beta)) - pow(k, (1-beta)))

else:

return (f - k) / log(f / k)

else:

return pow(k, beta)

cdef double _cy_zeta_over_x_of_zeta(double k, double f, double t, double alpha, double beta, double rho, double volvol):

"""Hagan's 2002 zeta / x(zeta) function - formulas (B.67a)-(B.67b)."""

cdef double eps = 1e-07 # Numerical tolerance for zeta

cdef double f_av = sqrt(f * k)

cdef double zeta = volvol * (f - k) / (alpha * pow(f_av, beta))

if abs(zeta) > eps:

return zeta / _cy_x(rho, zeta)

else:

# The ratio converges to 1 when zeta approaches 0

return 1.

cdef double _cy_x(double rho, double z):

"""Hagan's 2002 x function - formula (B.67b)."""

cdef double a = sqrt(1 - 2*rho*z + z*z) + z - rho

cdef double b = 1 - rho

return log(a / b)

cpdef double cy_normal_vol(double k, double f, double t, double alpha, double beta, double rho, double volvol):

"""Hagan's 2002 SABR normal vol expansion - formula (B.67a)."""

# We break down the complex formula into simpler sub-components

cdef double f_av = sqrt(f * k)

cdef double A = - beta * (2 - beta) * alpha*alpha / (24 * pow(f_av, (2 - 2 * beta)))

cdef double B = rho * alpha * volvol * beta / (4 * pow(f_av, (1 - beta)))

cdef double C = (2 - 3 * rho*rho) * volvol*volvol / 24

cdef double FMKR = _cy_f_minus_k_ratio(f, k, beta)

cdef double ZXZ = _cy_zeta_over_x_of_zeta(k, f, t, alpha, beta, rho, volvol)

# Aggregate all components into actual formula (B.67a)

cdef double v_n = alpha * FMKR * ZXZ * (1 + (A + B + C) * t)

return v_n

cpdef double cy_call(double K, double F, double T, double A, double alpha, double beta, double rho, double volvol):

cdef double iv = cy_normal_vol(K, F, T, alpha, beta, rho, volvol)

cdef double d = (F-K)/(iv*sqrt(T))

return A*iv*sqrt(T)*(norm.pdf(d) + d*norm.cdf(d))

cpdef double cy_put(double K, double F, double T, double A, double alpha, double beta, double rho, double volvol):

return cy_call(K, F, T, A, alpha, beta, rho, volvol) + A*(K-F)

@interact(F=(0.08, 0.15, 0.001), T=(1, 5, 1), alpha=(0.001, 0.01, 0.001), beta=(0.01, 0.99, 0.1), rho=(-0.99, 0.99, 0.1), volvol=(0.01, 1, 0.1))

def plot(F=0.1, T=1, alpha=0.01, beta=0.6, rho=0., volvol=0.6):

a = 0.08

b = 0.12

fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(16, 5))

ax1.plot([(K, cy_normal_vol(K, F, T, alpha, beta, rho, volvol)) for K in np.arange(a, b, 0.01)])

ax1.set(ylim=(-0.001, 0.015), title='SABR Normal Implied Vol')

ax2.plot([(K, cy_call(K, F, T, 1., alpha, beta, rho, volvol) if K>F else cy_put(K, F, T, 1., alpha, beta, rho, volvol)) for K in np.arange(a, b, 0.001)])

ax2.set(ylim=(-0.0001, 0.0012), title='OTM Option PV')

plt.show()

Boundary Condition for SABR PDE at \(\alpha_{\max}\)

Shreve p.289:若 \(c(t, S_t, V_t)\) 為 Heston model 下的 call PV,則 \begin{align*} \lim_{v\rightarrow \infty} c(t, s, v) = s \qquad\forall~0\le t\le T, s\ge 0. \end{align*}

當 vol 很大時 Heston model 退化為 Black-Scholes model 且 \(d_1\rightarrow \infty\), \(d_2\rightarrow -\infty\),於是 Black-Scholes call formula 退化為 \(S_0\)

同理 vol 很大時 Black-Scholes put formula 退化為 \(Ke^{-rT}\)

一般 SV model 當 vol 很大時都會退化為 constant vol model

以 \(\beta=0\) 的 SABR model 為例 \begin{align*} \begin{cases} dF_t = \alpha_tdW_t, \\ \alpha_t = \alpha e^{-\frac{\nu^2}{2}t + \nu Z_t} \end{cases} \end{align*} We have \begin{align*} F_T &= F_0 + \int_0^T \alpha_t\,dW_t = F_0 + \alpha \int_0^T e^{-\frac{\nu^2}{2}t + \nu Z_t}\,dW_t, \\ E\left[(F_T - K)^+\right] &= E\left[ \left(F_0 + \alpha \int_0^T e^{-\frac{\nu^2}{2}t + \nu Z_t}\,dW_t - K\right)^+\right], \end{align*} while constant vol model is \(d\bar F_t = \alpha dW_t\), \begin{align*} E\left[(\bar F_T - K)^+\right] &= E\left[ \left(F_0 + \alpha W_T - K\right)^+\right]. \end{align*}

直觀上,當 \(\alpha\) 很大時 \(\alpha\int_0^T e^{-\frac{\nu^2}{2}t + \nu Z_t}\,dW_t\) 和 \(\alpha W_T\) 都是很寬的對稱分布(對稱於 0),所以兩個期望值會很接近

若要嚴僅可以計算 \(F_T\) 的各階 moment

constant vol model: \(\bar F_T = F_0 + \alpha W_T\)

SABR with \(\beta=0\): \(dF_t = \alpha_t dW_t\), \begin{align*} &dF_t^2 = 2F_tdF_t + \alpha_t^2dt\\ \Longrightarrow\quad& F_T^2 - F_0^2 = \int_0^T 2F_t\alpha_t\,dW_t + \int_0^T\alpha_t^2\,dt\\ \Longrightarrow\quad& \text{Var}(F_T) = E\left[F_T^2\right] - F_0^2 = \int_0^TE\left[\alpha_t^2\right]\,dt, \end{align*} where \(\alpha_t\) is log-normally distributed and all moments are known in closed form.

計算 moment 的 argument 對 \(\beta\neq 0\) 不適用,對 Heston 適用,一般 SV model 不適用。當 dynamics 不是 affine process 連 2nd moment 都算不出來

直觀上 vol 越大 call PV 要越大,但超過 \(S_0\) 會產生 arbitrage,於是就有 \begin{align*} \lim_{v\rightarrow \infty} c(t, s, v) = s \qquad\forall~0\le t\le T, s\ge 0. \end{align*}

同理 vol 越大 put PV 要越大,但超過 \(Ke^{-rT}\) 會產生 arbitrage 所以 \begin{align*} \lim_{v\rightarrow \infty} p(t, s, v) = Ke^{-rT} \qquad\forall~0\le t\le T, s\ge 0. \end{align*}

如果 \(c > S_0\) 時的 arbitrage:

Sell call at \(c\) and buy underlying at \(S_0\) 得到正現金流

到期若被 assign,拿手上的 underlying 去 deliver

如果 \(p > Ke^{-rT}\) 時的 arbitrage:

Sell put at \(p\) and set aside \(Ke^{-rT}\) in MMA 得到正現金流

到期若被 assign,拿 MMA 裡的 \(\$K\) 買下 underlying

More on \(\alpha_{\max}\)

Note that \(\alpha_t\) follows a lognormal process \(d\alpha_t = \nu \alpha_t dZ_{t}\) so

If we want \(P(\alpha_T > \alpha_{\max}) \le \delta\), then

More on Limiting Case at \(\alpha_{\max}\)

Take expectation on both sides of \((F_T - K)^+ = (F_T - K) + (K - F_T)^+\) to get \begin{align*} V_0 &= f - K + E[(K - F_T)^+]\\ &= f - KP(F_T > K) - KP(K\ge F_T) + E[(K - F_T)^+]\\ &= f - KP(F_T > K) - E[F_T \cdot \mathbb 1_{\{K\ge F_T\}}]\\ \end{align*}

對於 \(K P(F_T > K)\):當波動率極大時,為了維持 \(E[F_T] = f\) 這個常數,分佈必須極度向左偏(Mass 集中在 0 附近)以抵消右側極端長尾的貢獻。因此,結束在 \(F_T > K\) 的機率測度 \(P(F_T > K)\) 會趨近於 \(0\)

對於 \(E[F_T \cdot \mathbb{1}_{\{F_T \le K\}}]\):這一項描述的是「當標的價格落在 \([0, K]\) 區間時的價值期望值」。當 \(\alpha \to \infty\) 時,標的價格 \(F_T\) 幾乎以機率 1 趨近於 0(即便它有極小的機率噴發到天文數字)。在 \([0, K]\) 這個有限區間內,\(F_T\) 的貢獻度會被壓制到趨近於 \(0\)

BCs in Heston and SABR

Boundary |

Heston (\(s, v\)) |

SABR (\(f, \alpha\)) |

物理與數值含義 |

|---|---|---|---|

Asset Low |

\(c(t, 0, v) = 0\) |

\(V(t, 0, \alpha) = 0\) |

標的價格為 0 時,買權價值為 0 |

Vol Low |

\(c(t, s, 0) = (s - Ke^{-r\tau})^+\) |

\(V(t, f, 0) = (f - K)^+\) |

波動率為 0 時,期權價值等於其內在價值 |

Asset High |

\(\frac{\partial^2 c}{\partial s^2} \to 0\) or \(c \approx s - Ke^{-r\tau}\) |

\(\frac{\partial^2 V}{\partial f^2} \to 0\) or \(V \approx f - K\) |

當標的價格極高,期權進入深價內,Gamma 趨近於 0 |

Vol High |

\(c(t, s, v) \to s\) |

\(V(t, f, \alpha) \to f\) |

當波動率無限大,標的覆蓋行使價的機率極高,價值趨近標的資產 |

SABR Forward Equation

Let \(\sigma = \log\alpha\). When \(\beta = 0\), the forward equation is

When \(\beta > 0\), with \(z_t = F_t^{1-\beta}/(1-\beta)\), the forward equation is

and the matrix will have huge condition number. Apply the Gauge Transform \(p(z, \sigma) = z\psi(z, \sigma)\) to obtain

All zero Dirichlet BCs can longer be used. Instead, one should use a Robin condition at \(z=0\)

One can still list a system of ODEs with constant matrix \(A\)

Dollar-Cost Averaging in Black-Scholes